ACF2100 Lecture 8: Lecture 8 Note – Extractive Industries

3 Aug 2018

School

Department

Course

Professor

Document Summary

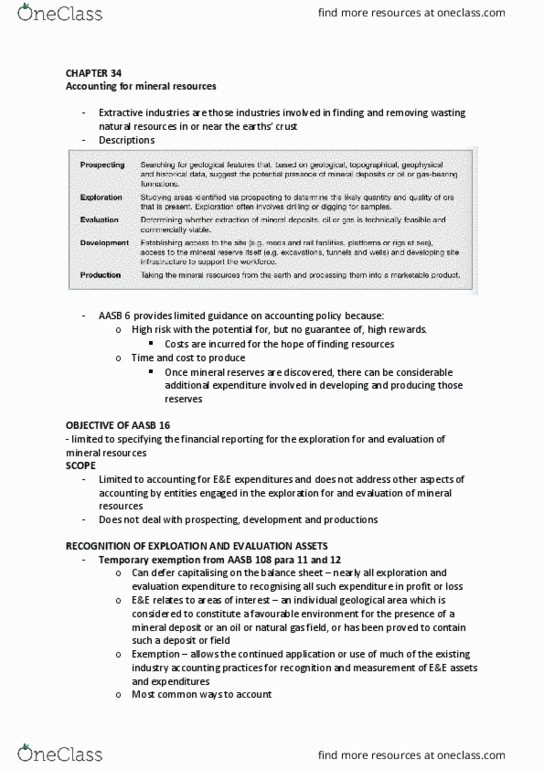

Aasb 6 exploration for and evaluation of mineral resources. Extractive industries are exploration, production, sale of, non-renewable natural resources such as minerals, oil and natural gas. Long period to exploit the deposit fully. Aasb 6 activiites-based standard dealing solely with treatment of costs of exploration and evaluation. Development and construction costs must apply other standards. Amortization of capitalized costs aasb 116. Restoration costs aasb 137, 116, and interpretation 1. The nature of the accounting problem in the extractive industries. Exploration of areas lease for this purpose. Possible construction of facilities for extraction, treatment and transportation from the deposit or field. Costs surveys, salaries, supplies, use of equipment, payment to property owners for access. Stage 1: exploration - includes the topographical, geological, geochemical and geophysical studies that are usually made over a wide area. Costs salaries and wages, supplies, transport, depreciation, rentals etc. Stage 2: evaluation - work is undertaken to determine the technical feasibility and commercial viability of the prospect.