ACC1100 Lecture 12: Acc1100 = W12 = Critical Analysis

8 Aug 2018

School

Department

Course

Professor

Document Summary

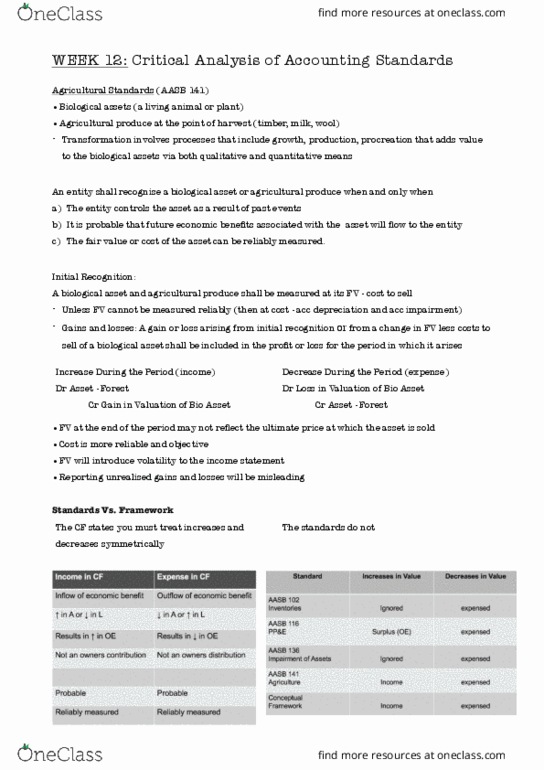

Biological assets = assets that are a living plant or animal. Agricultural produce = the harvested product from a biological asset. Transformation = involves processes that include growth, production and procreation that adds value to the biological assets via both quantitative and qualitative means. Biological product > agricultural product > products that result after processing the harvest. Sugar cane (the crop) > harvested cane > sugar. An entity should recognise a biological asset or agricultural asset when and only when: The entity controls the asset as a result of past events. It is probable that future economic benefits associated with the asset will flow to the entity and. The fair value or cost of the asset can be reliably measured. This adopts the definition and recognition criteria provided in the aasb framework. Biological assets can increase or decrease in value from: its initial recognised value or, a change of fair value less costs to sell: