ACF1200 Lecture Notes - Lecture 8: Accounts Receivable

2 Aug 2018

School

Department

Course

Professor

Document Summary

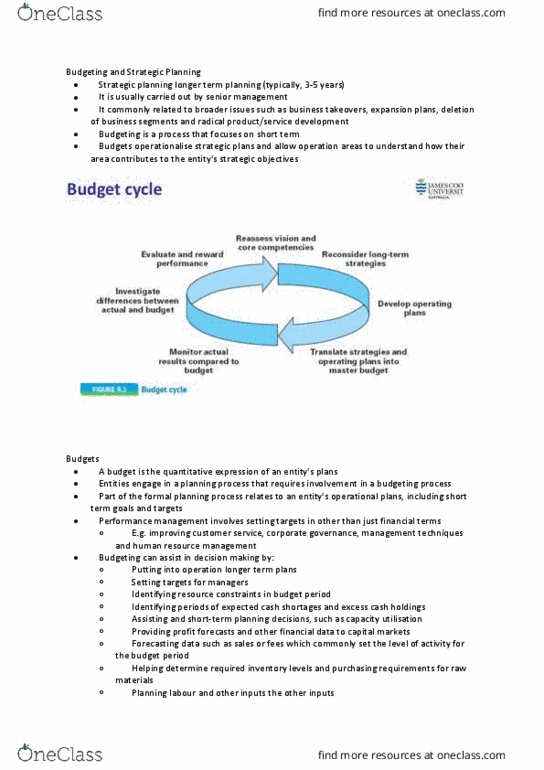

Budgets are plans, expressed in monetary terms, for a future period. They serve as a control mechanism to monitor actual results and investigate differences that arise between actual and budget. Actual results are compared to budgets to identify variances. They help in evaluating performance and promote ef ciency. Management can use them to determine whether or not business objectives have been met. Fixed budget: annual budget, does not often change for the year. The budgeting process: consider past performance, assess expected trading and operating conditions, prepare initial estimates, communicate with managers and adjust estimates o prepare budgets, monitor performance against budget, adjust budgets if necessary. Statement of expected future cash receipts and payments. Useful if prepared in short time intervals such as monthly. Projects what the cash balance will be in the future. If a cash budget forecasts a de cit, arrangements can be made to avoid it. If a cash budget forecasts a surplus, investment opportunities can be considered.