AYB301 Lecture Notes - Lecture 2: Financial Institution, Internal Audit, Internal Control

Document Summary

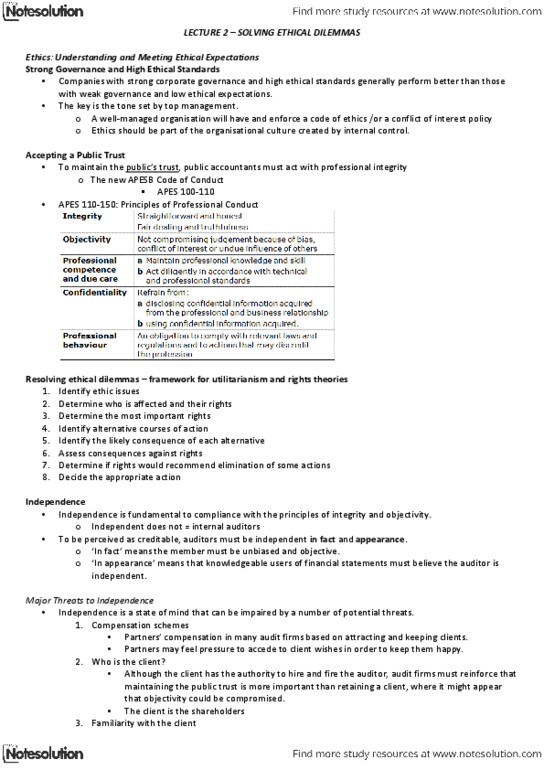

Lecture 2 solving ethical dilemmas: companies with strong corporate governance and high ethical standards generally perform better than those with weak governance and low ethical expectations. The key is the tone set by top management: a well-managed organisation will have and enforce a code of ethics /or a conflict of interest policy, ethics should be part of the organisational culture created by internal control. To maintain the public"s trust, public accountants must act with professional integrity: the new apesb code of conduct. Apes 100-110: apes 110-150: principles of professional conduct. Resolving ethical dilemmas framework for utilitarianism and rights theories. Identify ethic issues: determine who is affected and their rights, determine the most important rights. Identify the likely consequence of each alternative: assess consequences against rights, determine if rights would recommend elimination of some actions, decide the appropriate action. Independence is fundamental to compliance with the principles of integrity and objectivity.