AYB200 Lecture Notes - Lecture 12: Income Statement, Trial Balance, General Ledger

Lecture 12: Cash Flow Statement

Financial Statements

Purpose of CFS

- Assist in assessing the ability of the company or economic entity to:

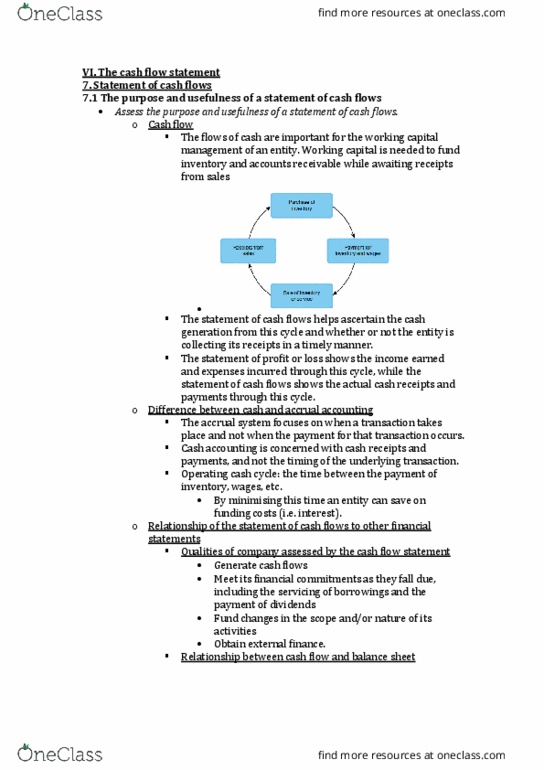

o Generate cash flows

o Meet financial commitments as they fall due, including servicing of borrowings and

payment of dividends

o Fund changes in the scope and/or nature of its activities

o Obtain external finance

o By having knowledge of both cash flows and accrual of profits/losses, investors are

likely to be better able to assess the performance and viability of the reporting

entity

o Argued (by some people) to be more reliable than profit data as profit data typically

ased o ueous sujetie ad soeties eatie judgets

o Cash-flo data teds to e oe fatual o ojetie

o Considered by many to be more understandable to users, to give rise to fewer

problems with key terms, and to provide greater comparability between companies

o Cash flows from operations are considered (by some people) to be a superior

performance measure and useful in assessing liquidity and solvency

Why CF Matters

- 80% of small businesses fail within the first three years

- The Top reason for failure is cash flow problems

AASB107: Cash Flow Statements

- Objectives of AASB 107 (preamble):

o to euie the poisio of ifoatio aout the histoial hanges in cash and

cash equivalents of an entity by means of a cash flow statement which classifies cash

flos duig the peiod fo opeatig, iestig ad fiaig atiities

AASB Definitions

- Cash flos: iflos ad outflos of ash ad ash euialets paa 6

find more resources at oneclass.com

find more resources at oneclass.com

- Cash: on hand (notes and coins held) and demand deposits (deposits on call with financial

institutions)

- Cash equivalents:

- shot-term, highly liquid investments that are readily convertible to known amounts of cash

and which are subject to a isigifiat isk of hages i alue paa 6

Cash Flow Statement Format

Cash Flow Statements: Operating Activities

Interest and Dividends

find more resources at oneclass.com

find more resources at oneclass.com

Cash Flow Statements: Investing Activities

Cash Flow Statements: Financing Activities

Operating Cash Flows: Choice of Method

- Operating cash flows may be reported using one of two methods (para 18):

- Direct method:

o Major classes of gross cash receipts and payments are disclosed.

o Para 19 encourages this method. We will use this method!

- Indirect method:

o profit or loss is adjusted for the effects of transactions of a non-cash nature,

deferrals or accruals etc).

o Determine net cash flows from operating activities by adjusting profit or loss for

effects of

o Changes in inventories and operating receivables and payables

o Non-cash items (e.g. depreciation, provisions etc)

o All other items for which cash effects are investing or financing cash flows

Cash Flow Statements: Preparation

- Cash flow is NOT prepared from the general ledger trial balance

o Unlike balance sheets and income statements

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

80% of small businesses fail within the first three years. The top reason for failure is cash flow problems. Cash flo(cid:449)s: (cid:862)i(cid:374)flo(cid:449)s a(cid:374)d outflo(cid:449)s of (cid:272)ash a(cid:374)d (cid:272)ash e(cid:395)ui(cid:448)ale(cid:374)ts(cid:863) (cid:894)pa(cid:396)a 6(cid:895) Cash: on hand (notes and coins held) and demand deposits (deposits on call with financial institutions) Cash equivalents: (cid:862)sho(cid:396)t-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to a(cid:374) i(cid:374)sig(cid:374)ifi(cid:272)a(cid:374)t (cid:396)isk of (cid:272)ha(cid:374)ges i(cid:374) (cid:448)alue(cid:863) (cid:894)pa(cid:396)a 6(cid:895) Operating cash flows may be reported using one of two methods (para 18): Direct method: major classes of gross cash receipts and payments are disclosed, para 19 encourages this method. Cash flow is not prepared from the general ledger trial balance: unlike balance sheets and income statements. Comparative balance sheets are often used, with supplementary information from the income statement and specific general ledger transactions.