ACC10007 Lecture Notes - Lecture 5: Financial Analysis, Financial Statement, Market Sentiment

Document Summary

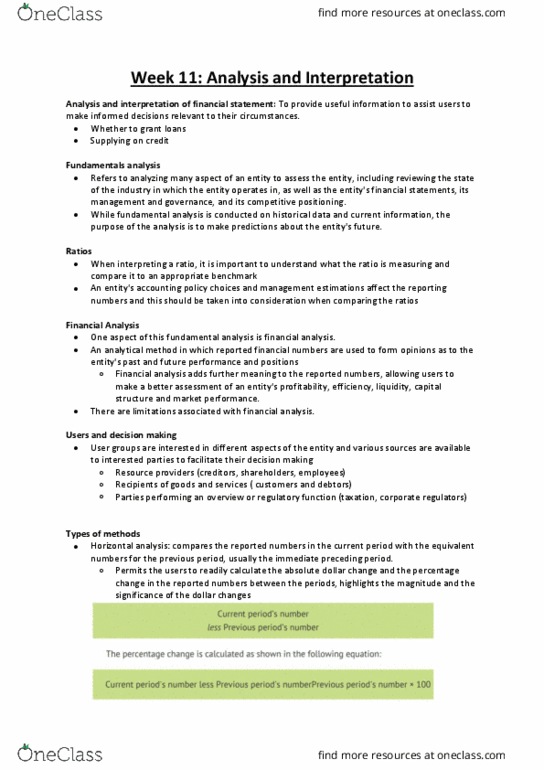

Users of financial information can be categorised as resource providers (for example. Creditors, lenders, shareholders and employees); receipts of goods and services (e. g customers and debtors); and parties performing an overview or regulatory function (e. g the taxation office, corporate regulators, or a statistical bureau). User groups are interested in different aspects if the entity, and various information sources are available to interested parties to facilitate their decision making. Another important source of information is financial statements. Therefore, with a knowledge and understanding of information contained in financial statements, financial analysis can provide information specific to the users needs. Financial analysis is an analytical method in which reported financial numbers are used to form opi(cid:374)io(cid:374)s as to the e(cid:374)tit(cid:455)(cid:859)s past a(cid:374)d future perfor(cid:373)a(cid:374)(cid:272)e a(cid:374)d positio(cid:374). Describe the purpose and nature of financial analysis. To express reported numbers in relation to other enabling relationships to be revealed and the fi(cid:374)a(cid:374)(cid:272)ial state(cid:373)e(cid:374)ts to tell a stor(cid:455) a(cid:271)out the e(cid:374)tit(cid:455)(cid:859)s fi(cid:374)a(cid:374)(cid:272)ial health.