BUSI 3008 Lecture Notes - Lecture 1: Croatian Radiotelevision, Income Statement, Pro Rata

6 Dec 2016

School

Department

Course

Professor

Document Summary

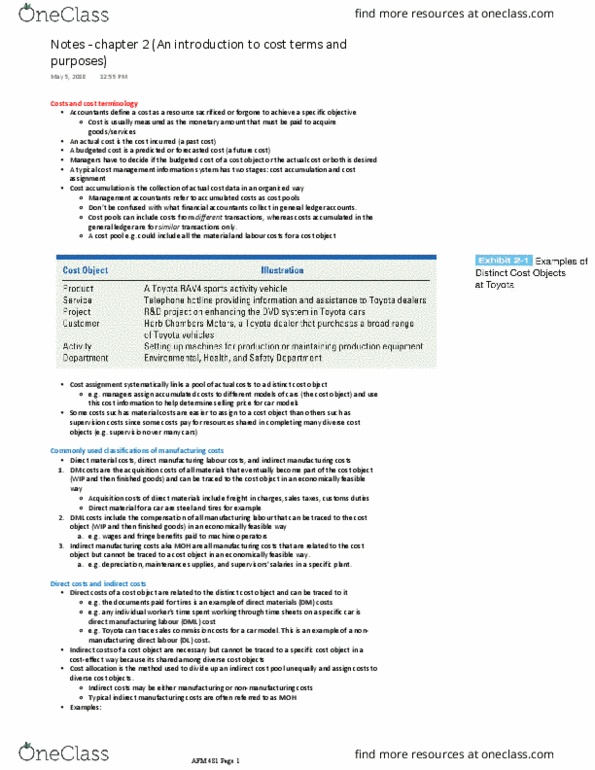

Chapter 1 accountant"s vital role in decision making. Measures and reports financial & non-financial info that is related to the costs of acquiring and using resources. Uses different methods to calculate how much it costs to make products. Goal: reporting and analyzing costs to make decisions to improve the business cost control & efficiency. Cost management system (2 stages: cost accumulation stage: all actual cost data is collected & organized into different cost pools, cost assignment stage: link actual cost to a cost object. Direct cost: can be traced to a cost object. Indirect cost: cannot be traced to a cost object. Direct costs: coffee beans, sugar, milk, cup, salary of employee. Indirect costs: factory/works overheads, admin. overheads, selling & distribution overheads. Direct material (dm): parts, raw materials, freight, duties, etc. Indirect manufacturing overhead (moh): maintenance supplies, lubricants, factory costs. Variable costs (vc): change proportionately with changes in activity levels remain constant on a per unit basis: ex.