ECON 1000 Lecture Notes - Lecture 13: W. M. Keck Observatory, Marginal Cost, Lemonade

16 Nov 2016

School

Department

Course

Professor

Document Summary

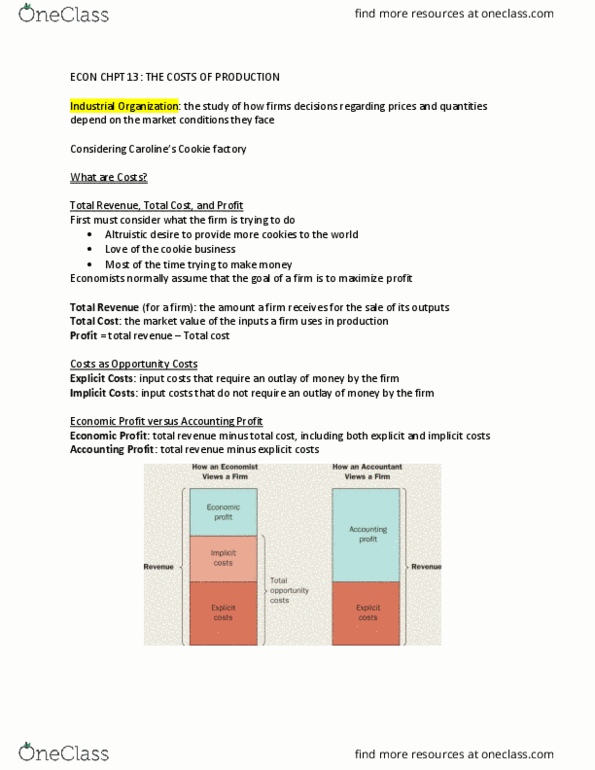

So far have assumed firms will supply a good if the price exceeds their cost of production. Now start to look at firm decisions in more detail. Move away from assumptions of many firms and consider other possibilities. Before we do look at the costs of production. Helen uys cookie ingredients, flour, sugar etc. Also buys mixers, ovens, hires workers etc. Helen"s business issues shed lights on firm costs in general. Assume firm objective is to maximize profit. Firm profit = total revenue - total costs. Total revenue is just price times quantity. Cost of something is what you give up to get it. Explicit costs , e. g. spent on flour, wages to workers etc. Implicit costs don"t require a cash outlay. This is a difference between how economics and accountants analyze a business. Economist interested in how firms make production and pricing decisions. Accountant tracks money in and money out.