ACCT-1001EL Lecture Notes - Lecture 1: Double-Entry Bookkeeping System, Retained Earnings, Accounting Information System

20 Jun 2018

School

Department

Course

Professor

January 17, 2018

Accounting Lecture 2 — Chapter 3

Summary

1. Explain how the double -entry accounting system works, including how it overcomes

the limitations of the temple approach.

-Every transaction must be recorded in a way that affects at least 2 accounts, with the effects

of these entries being equal and offsetting

-The double-entry accounting system enables the use of a huge number of accounts and is

not limited to a fixed number of columns as is the case with the template approach. This

allows the company to capture the information at the level of detail required to manage the

business, yet make it east to summarize the information for reporting purposes.

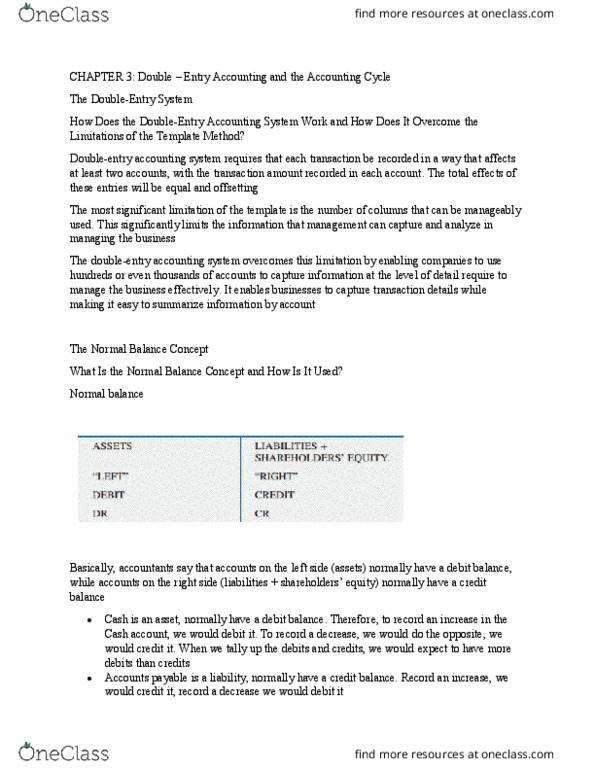

2. Explain the normal balance concept and how it is used within the double-entry

accounting system.

-The normal balance concept is used to determine whether an account normally has a debit to

credit balance.

-To determine an account’s normal balance, a “T” is drawn through the middle of the

accounting equation. Accounts on the left side of the “T” (assets) normally have a debit (DR)

balance, while accounts on the right side of “T” (liabilities and SE) normally have a credit (CR)

balance.

-An accounts normal balance illustrates what needs to be done to increase that account. The

opposite is don't to decrease it

-As retained earnings is a shareholders’ equity account, it normally has a credit balance.

Therefore, to increase it, we would credit it, and to decrease it, we would debit it.

-Following this, revenue accounts, which ultimately increase retained earnings, normally have

a credit balance. Expense and dividends declared accounts, which ultimately decrease

retained earnings, normal have a debit balance.

3. Identify and explain the steps in the accounting cycle.

The steps of the accounting cycle;

1. Start with opening balances

2. Complete transaction analysis

3. Record transactions in the general journal

4. Post transactions to the general ledger

5. Prepare a trail balance

6. Record ad post adjusting entries

7. Prepare an adjusted trial balance

8. Prepare financial statements

9. Prepare closing entries

-At a minimum this cycle is repeated annually, but parts of it repeat much more frequently

(quarterly, monthly, weekly or even daily)

find more resources at oneclass.com

find more resources at oneclass.com

January 17, 2018

4. Explain the significance of a company’s decision regarding its chart of accounts and

the implications of subsequent changes.

-The chart of accounts outlines the type of information management wishes to capture to

assist them in management the business

-The chart of account sis dynamic and can be changed when the company enters into new

types of operations, opens ne location, requires more detailed information or requires less

detailed information

5. Explain the difference between permanent and temporary accounts

-Permanent accounts have balances that are carried over from one accounting period to the

next

-Temporary accounts have absences that are closed to retained earning at the end of each

accounting period. That is, they are reset to zero

-All of the accounts on the statement of financial position (assets, liabilities, and shareholders

equity accounts) are permanent accounts

-All of the accounts on the statement of income (revenues and expenses) and dividends

declared are temporary accounts.

6. Identify and red transactions in the general journal and general ledger

-The general journal is chronological listing of all transactions. It contains detailed information

on each transaction

-Each journal entry must affect 2 or more accounts and the total dollar amount of debits in the

entry must be equal to the total dollar amount of credits. In other words, total DR = total CR.

-On a periodic basis (such as daily, weekly or monthly), the information record in the general

journal is posted to the general ledger

-The general ledger is used to prepare summary information for each account. The detail form

each journal entry affecting a specific amount is recorded in the general ledger account for

that specific account

-A trial balance is prepared to ensure that the total of all debits posted to the general ledger is

equal to the total of credits posted.

7. Explain why adjusting entries are necessary and prepare them.

-Adjusting entries are required at the end of each accounting period to record transactions that

may have been missed.

-There are 2 types of adjusting entries: accruals and deferrals

-Accrual entries are used to record revenues or expenses before cash is received oror paid

-Deferral entries are used to record revenues or expenses after cash has been received or

paid

-Depreciation is a type of deferral entry

-Adjusting entries never involve cash

find more resources at oneclass.com

find more resources at oneclass.com

January 17, 2018

8. Explain why closing entries are necessary and prepare them!

-Closing entries are used to close temporary accounts and transfer the balances in these

accounts to retained earnings

-There are four closing entries;

1. Close all revenue accounts to the Income Summary Account

2. Close all expense accounts to the Income Summary Account

3. Close the Income Summary Account to Retained Earnings

4. Close dividends Declared to Retained Earnings

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Summary: explain how the double -entry accounting system works, including how it overcomes the limitations of the temple approach. Every transaction must be recorded in a way that affects at least 2 accounts, with the effects of these entries being equal and offsetting. The double-entry accounting system enables the use of a huge number of accounts and is not limited to a xed number of columns as is the case with the template approach. The normal balance concept is used to determine whether an account normally has a debit to credit balance. To determine an account"s normal balance, a t is drawn through the middle of the accounting equation. Accounts on the left side of the t (assets) normally have a debit (dr) balance, while accounts on the right side of t (liabilities and se) normally have a credit (cr) balance. An accounts normal balance illustrates what needs to be done to increase that account.