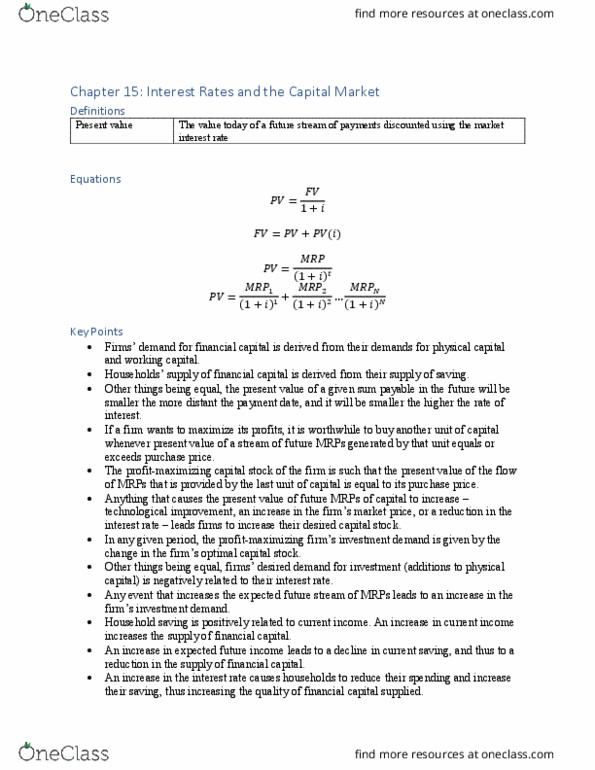

ECON-1006EL Lecture 15: In Class

24 views2 pages

16 Oct 2015

School

Department

Course

Professor

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Related Documents

Related Questions

| d. TTC recently introduced a new line of products that has been wildly successful. On the basis of this | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| success and anticipated future success, the following free cash flows were projected: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Year | FCF (in millions) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | $5.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2 | $12.1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3 | $23.8 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4 | $44.1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5 | $69.0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 6 | $88.8 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 7 | $107.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 8 | $128.9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 9 | $147.1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 10 | $161.3 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| After the 10th year, TTC's financial planners anticipate that its free cash flow will grow at a constant rate | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| of 6%. Also, the firm concluded that the new product caused the WACC to fall to 9%. The market value | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| of TTC's debt is $1,200 million, it uses no preferred stock, and there are 20 million shares of common | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| stock outstanding. Use the corporate valuation model approach to value the stock. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| INPUT DATA: (Dollars in Millions) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| WACC | 9% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| gn | 6% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Millions of shares | 20 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| MV of debt | $1,200 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Year | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | |||||||||||||||||||||||||||||||||||||||||||||||||

| FCF's | $5.5 | $12.1 | $23.8 | $44.1 | $69.0 | $88.8 | $107.5 | $128.9 | $147.1 | $161.3 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| PV of FCF's |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| PV of FCF1-10 = | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| HV at Year 10 of FCF after Year 10 = FCF11/(WACC â gn): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| PV of HV at Year 0 = HV/(1+WACC)10: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sum = Value of the Total Corporation | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less: MV of Debt and Preferred | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Value of Common Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of Shares (in Millions) to Divide By: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Value per Share = Value of Common Equity/No. Shares: | versus | using the discounted | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| dividend model | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The price as estimated by the corporate valuation method differs from the discounted dividends method because | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| different assumptions are built into the two situations. If we had projected financial statements, found both | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| dividends and free cash flow from those projected statements, and applied the two methods, then the | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| prices produced would have been identical. As it stands, though, the two prices were based on somewhat | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| different assumptions, hence different prices were obtained. Note especially that in the FCF model we | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| assumed a WACC of 9% versus a cost of equity of 10% for the discounted dividend model. That would obviously tend to | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| raise the price. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||