MGCR 211 Lecture Notes - Lecture 8: General Ledger, Cost Overrun, American Express

Document Summary

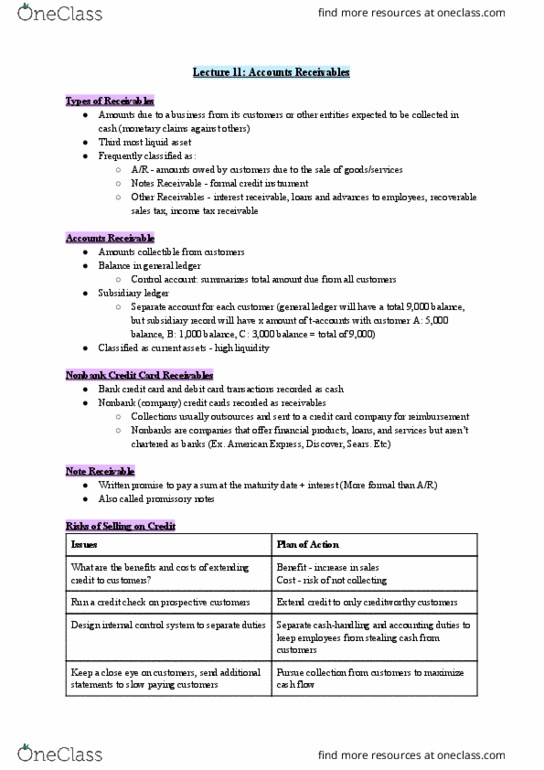

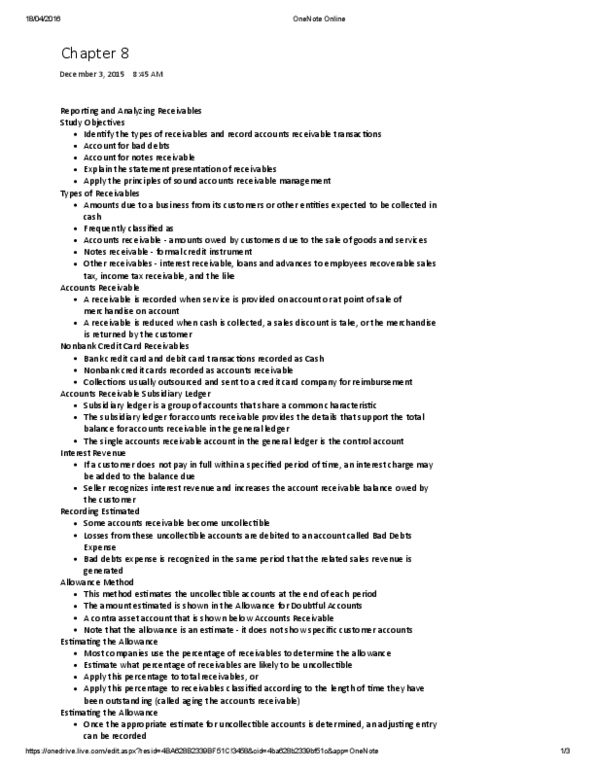

Balance in general ledger - control account: summarizes total amount due from all customers. Subsidiary ledger - separate account for each customer. Written promise to pay sum at maturity date. Benefits and costs of extending credit to consumers. Cost risk of not collecting employees can(cid:495)t steal. At the end of a period, companies will estimate bad debt expenses. Make estimate of the portion of accounts receivable that will not be collected (based on previous experiences), and allow for them at the same period when recording the sale. Estimate bad debt expense: amount of receivables expected not to be collected. Allowance for doubtful accounts (afda: contra account to a/r, credit balance account, balance sheet account. Computes bad debt expense as a percentage of net credit sales. Uncollectible expense = (estimated % uncollectible) x (net credit sales) Analyzes specific individual accounts receivable according to the length of time they have been outstanding.