MGCR 382 Lecture Notes - Lecture 7: Spot Contract, Interest Rate Parity, Arbitrage

13 Feb 2015

School

Department

Course

Professor

Document Summary

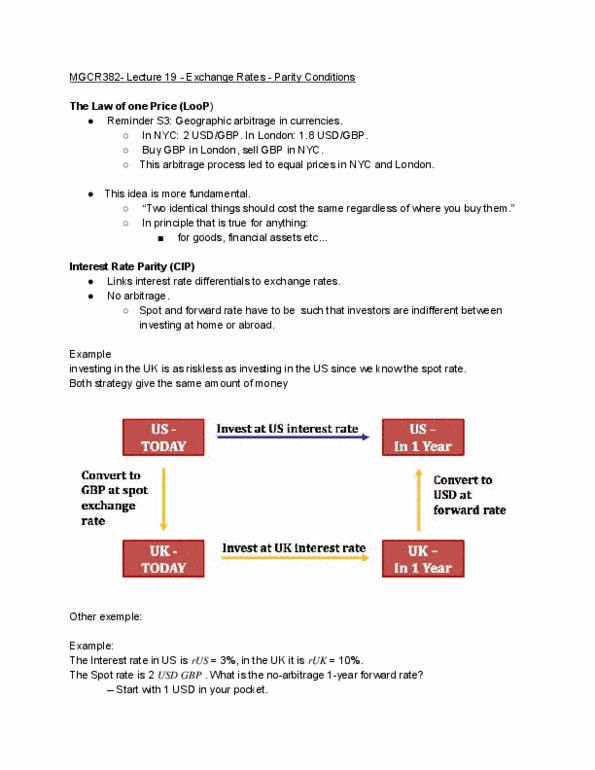

Mgcr 382- international business - lecture 7- parity conditions. States that in the real world, there are no real opportunities of arbitrage to occur. In other words, two identical things should cost the same regardless of where you buy them . Is the process that links interest rate differentials to the exchange rates: using the forward exchange rate", the company is able to cover" their risk probability, with regard to the exchange rate. Example of interest parity: a us dollar invested in us would give an interest rate of 0. 03, the same 1 us dollar invested in uk would give you an interest rate of 0. 10, to calculate the forward rate: Uncovered interest rates: hypothesis that aims to predict the future spot rate with the forward agreement, there no longer an idea of arbitrage; just speculation.