BUSI 1101 Lecture Notes - Lecture 4: Bank Reconciliation, General Ledger, Current Liability

13 Mar 2018

School

Department

Course

Professor

Document Summary

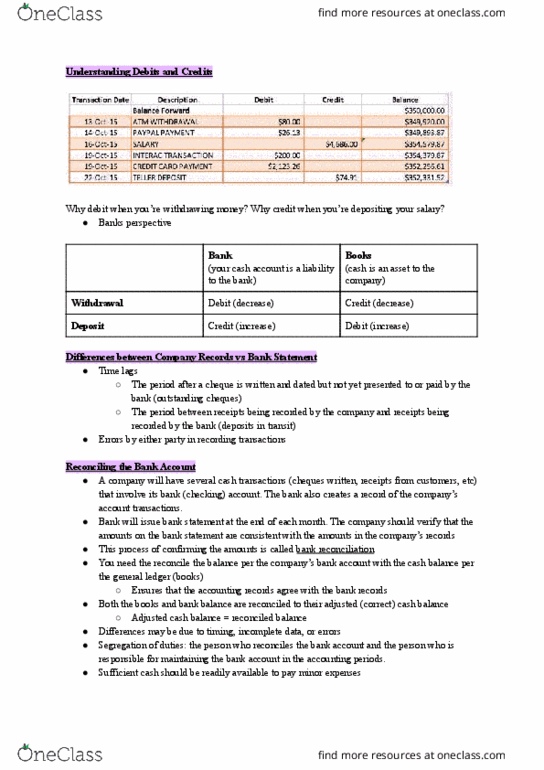

Safeguards cash by using a bank as a depository and clearinghouse for cheques received and written. Minimizes amount of currency that must be kept on hand. Provides a second record of transactions: one by the business, one by the bank. Errors by either party in recording transactions. This reconciles the balance per the company"s bank account with the cash balance per the general ledger ( books : makes them agree. Both the books and the bank balance are reconciled to their adjusted (corrected) cash balance: adjusted cash balance = reconciled balance. Books: each reconciling item in determining the adjusted balance per books must be journalized and posted. Bank: do not journalize any entries on bank sde. Cash is reported in both the statement of financial position and the statement of cash flows: statement of cash flows show the receipts and payments of cash.