FIN 305 Lecture Notes - Lecture 12: Net Profit, Net Income, Gross Profit

7 Dec 2015

School

Department

Course

Professor

Document Summary

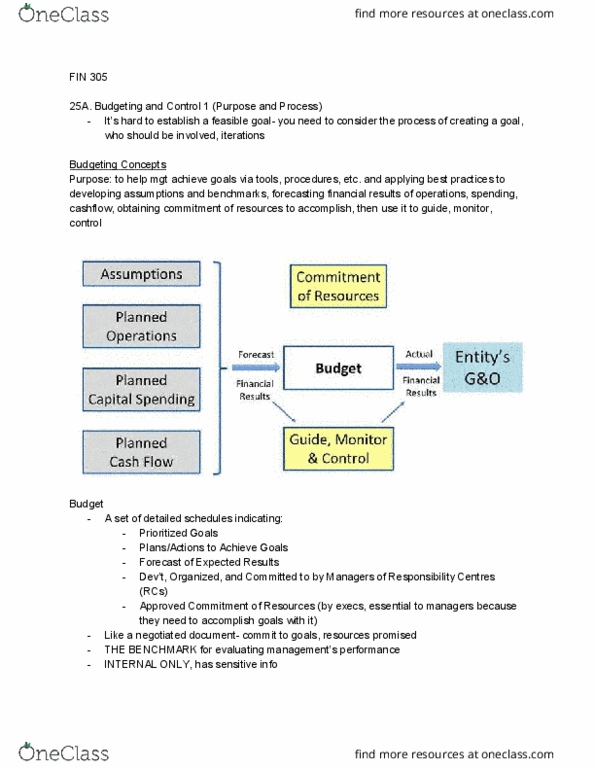

Planning, setting financial goals and objectives, marshalling resources and commitments to achieve them. 3 components: operating budget: reflects plans and decisions of operating activities. Divide period into intervals weekly monthly: capital budget: reflects decisions about capital expenditures ie. investing activities. Planned expenditures for long term resources and related financing. Focuses on investing assets/resources required to achieve planned goals that aren"t limited to short term. Can include replacement or renovation of assets. Productivity and improvement initiatives by buying new equipment. Explore alternative sources of funds in terms of availability, cost, flexibility. Longer term spanning 3-5 years depending on perceived reliability or uncertainty of operating budget. May be divided into quarters, particularly for the first 2 years and then annually. Gives responsibility centres some flexibility over when they actually spend their capital budgeted funds: cash budget: reflects decisions about cash management and consolidates cash consequences of both operating and capital budgets.