ACCT 1220 Lecture Notes - Lecture 9: Land Development, Intangible Asset, Asset

28 Nov 2017

School

Department

Course

Professor

Document Summary

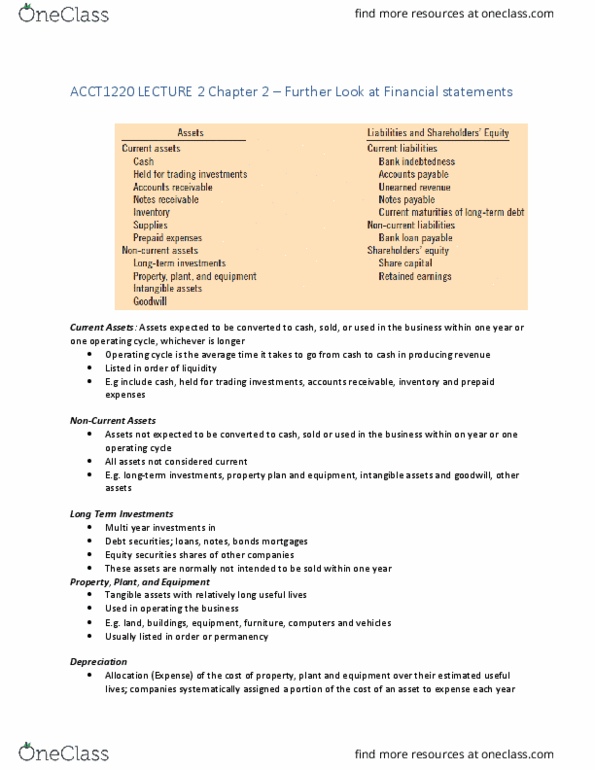

November 17 - reporting and analyzing long-lived assets. Used over more than one accounting period. Purchase price, include non-refundable taxes and duties, less discounts or rebates. Expenditures necessary to bring asset to its intended location and make it ready for its intense use. Estimated cost of future obligations to dismantle, remove or restore the asset at the end of its useful life. Types of expenditures what item you include in cost, di erentiate between the two. Capitalized as an long-live asset (increase cost of the asset) Increase a company"s investment in productive activity. Ex: purchase equipment is a capital expenditure because will bene t the future, insurance cost while being shipped is also induced in capital expenditure. But insurance paid after its situated is an expense because cost bene t current period. Closing costs such as title and legal fees. Additional costs to prepare land for its intended use (less proceeds from salvage) Recorded as capital expenditures on land account.