ECON 1050 Lecture Notes - Lecture 4: Economic Equilibrium, Demand Curve, Iller

Document Summary

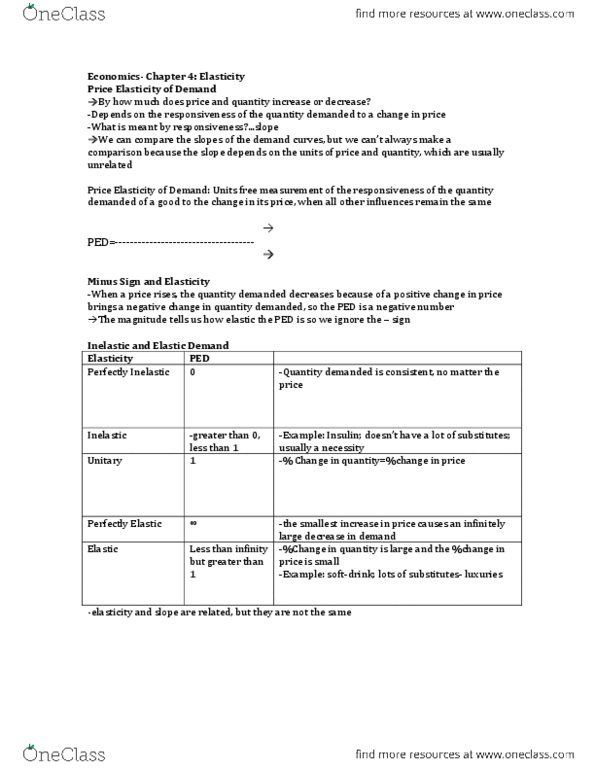

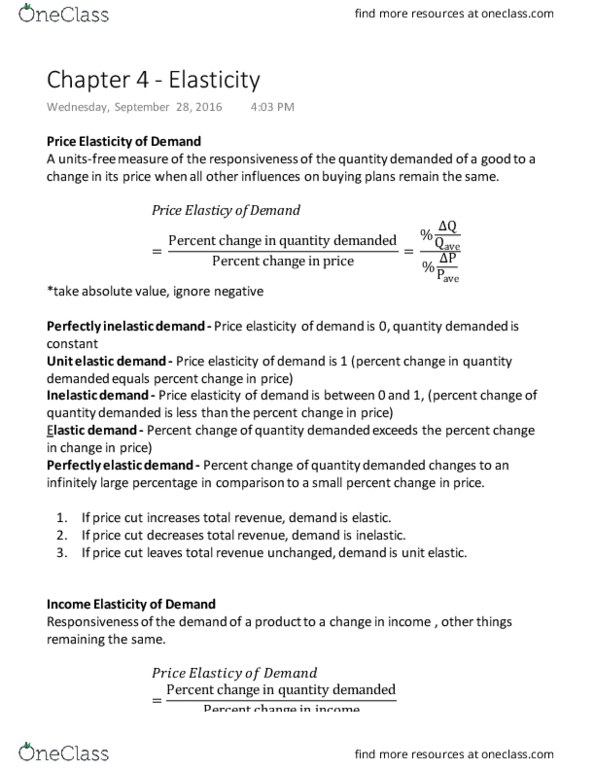

As supply decreases, the equilibrium price rises and the equilibrium quantity decreases. If quantity demanded is not responsive to change in price, price rises a lot and equilibrium quantity does not change much. If quantity demanded is very responsive to a change in price, price barely rises and the equilibrium quantity changes a lot. Demand curve flat = quantity demanded is very responsive. Price elasticity of demand: units free measure of the responsiveness of the quantity demanded of a good to a change in its price when all other influences on buying plans remain the same. Perfectly inelastic demand = quantity demanded remains constant when the price changes, price elasticity of demand is zero. Unit elastic demand = percentage change in the quantity demanded equals the percentage change in the price (price elasticity = 1) Inelastic demand = price elasticity of demand is between 0 and.