ECON 3660 Lecture Notes - Lecture 15: Idiosyncrasy, Capital Asset Pricing Model, Market Risk

14 Dec 2017

School

Department

Course

Professor

Document Summary

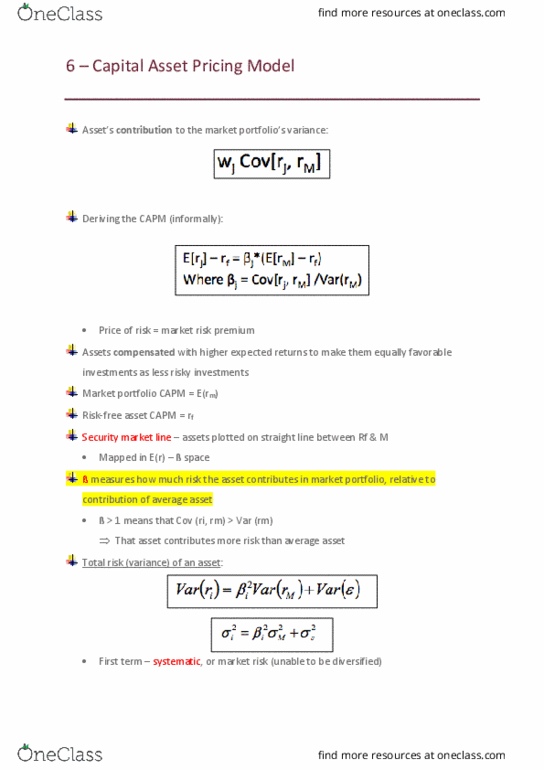

The capm is the only model we can prove. High beta assets will not perform well when you need them to (i. e. when the market goes down) Risk that is no systematic (market risk) is automatically idiosyncratic. You cannot observe idiosyncratic risk, you must calculate it by subtracting total risk by syncretic risk. You should find that if you build portfolios, idiosyncratic risk should go to zero. Across time, epsilon averages to zero or n given that n is very large (number of assets in the portfolio) How can i use the capm: estimate beta: get expected return. Prove: higher the risk higher the expected return. Decile portfolios: i. e. create 10 portfolios with ordered betas (so that portfolio 1 has lowest beta and portfolio 10 has the highest beta) Ken french does this for us (yay) portfolios ranked by beta.