AFM131 Lecture Notes - Lecture 12: Debenture, Initial Public Offering, Commercial Paper

2 May 2017

School

Department

Course

Professor

22

AFM131 Full Course Notes

Verified Note

22 documents

Document Summary

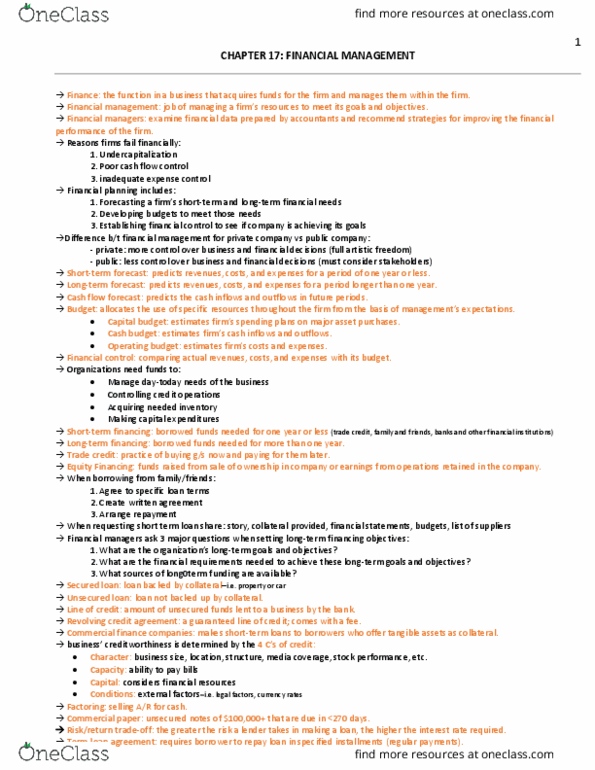

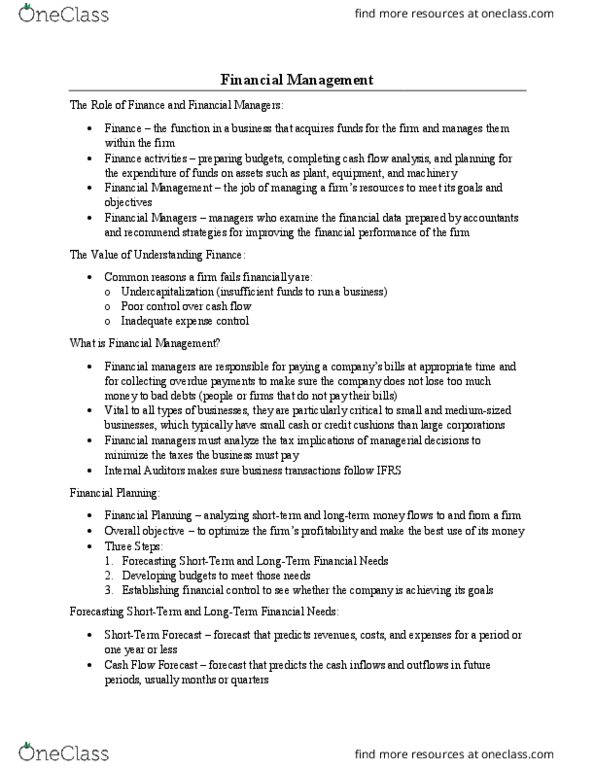

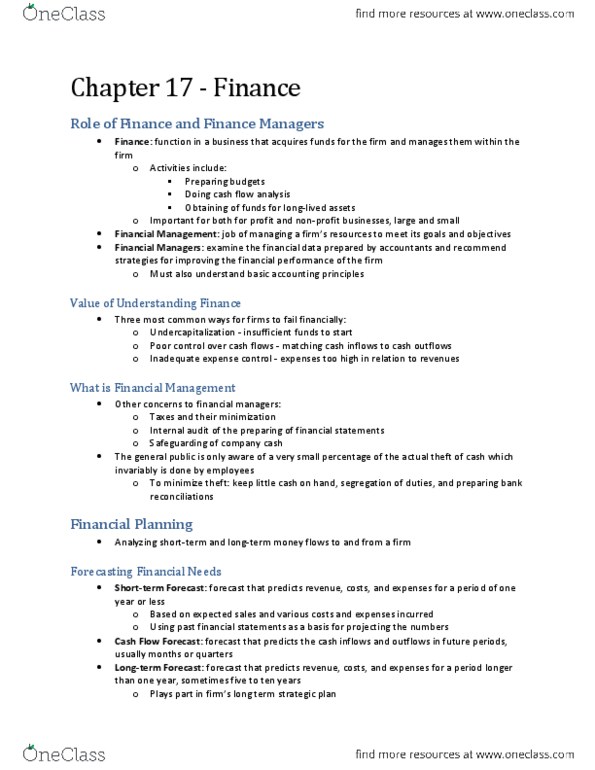

Finance: the function in a business that acquires funds for the firm and manages those funds within the. Financial management: the jo(cid:271) of (cid:373)a(cid:374)agi(cid:374)g a fir(cid:373)"s resour(cid:272)es so it (cid:272)a(cid:374) meet its goals and objectives. Financial managers: managers who make recommendations to top executives regarding strategies for improving the financial strength of a firm. Auditing, planning, budgeting, obtaining funds, controlling funds (fund management), collecting funds (credit management), advising top management on financial matters, managing taxes. 3 ways for firms to fail financially: undercapitalization (lacking funds to start and run a business, pool control over cash flow. Financial planning involves 3 steps: forecasting both short-term and long-term financial needs, developing budgets to meet those needs, establishing financial control to see how we ll the company is doing what it set out to do. Short-term forecast: forecast that predicts revenues, costs, and expenses for a period of 1 year or less. Part of this state(cid:373)e(cid:374)t is i(cid:374) the for(cid:373) of .