AFM351 Lecture Notes - Lecture 8: Audit Evidence, Audit Risk, Balance Sheet

4 Jul 2020

School

Department

Course

Professor

Document Summary

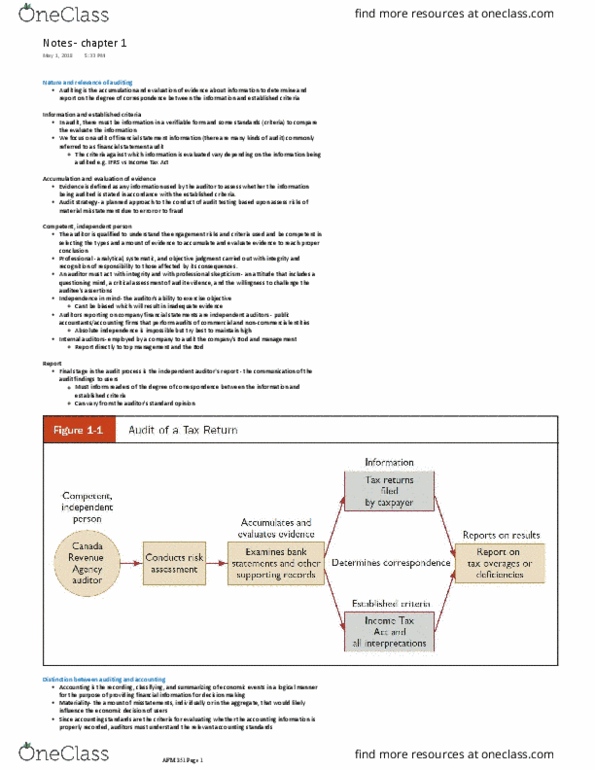

Audit evidence: information used by the auditor to form a conclusion on the audit opinion: absence of information is evidence, can indicate a problem. Sufficient and appropriate evidence: enough evidence (sufficient) that is of high quality (appropriate, high level of confidence that the conclusion is correct, timely. Appropriateness of evidence: connected to assertion (relevance, evidence is truthful (reliability, auditor"s direct knowledge is more reliable. Information from third party is more reliable than the information provided by the client: effectiveness of client internal controls, retaining and protecting good information, consistency from multiple sources. Select all items or sampling: significant accounts and significant amounts, how much is based on risk and nature of the evidence being collected. Timing: throughout the year and at the end of the year, more balanced evidence if collected throughout the year. Inspection/observation: higher reliability, done directly by auditor. Audit strategy: broad blueprint, audit risk, plan, procedures. Investigate the exception: determine how long the control was not working.