AFM362 Lecture Notes - Lecture 11: Economic And Monetary Union Of The European Union, Old Age Security, False Statement

28 Jun 2018

School

Department

Course

Professor

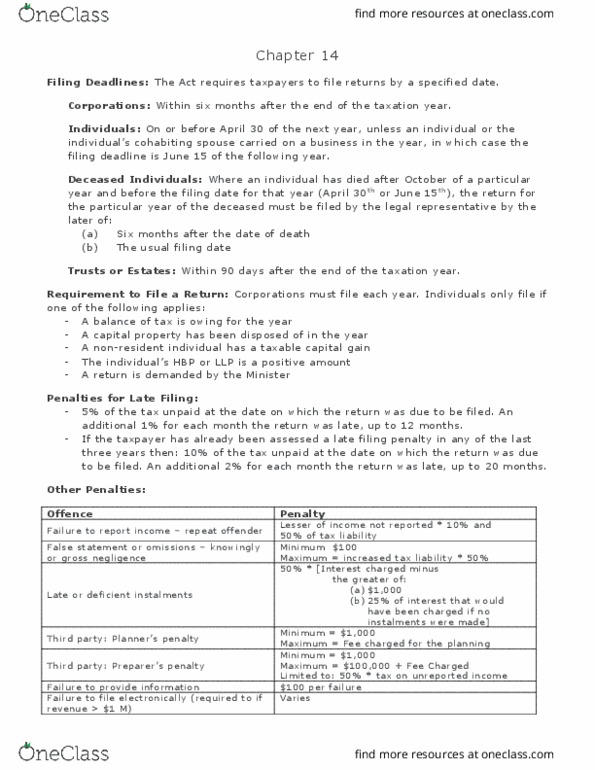

RETURNS

Corporations- within six months after the end of the taxation year (their fiscal year)•

Unless individual or spouse carried on a business then June 15th of the following year○

Individuals- on or before April 30th of the next year•

Six months after date of deatha)

The usual filing date (April 30 or June 15)b)

If dead outside of the time limit, the usual filing date apply○

Deceased individuals - if died after Oct and before April 30 or June 15 then must be the later of:•

Trusts or estates - within 90 days after the end of the taxation year•

Filing deadlines

Corporations must file each year in Canada•

A balance of tax is owing for the year○

A capital property has been disposed of in the year○

A non-resident individual has a taxable capital gain (e.g., claimed a capital gains reserve in the previous year)○

The individual's Home Buyer Plan (HBP) balance or Lifelong Learning Plan (LLP) is a positive amount○

A return is demanded by the Minister○

Individuals must file only if one of the following applies:•

Individuals with a refund due should file•

Low income taxpayer should file to receive income-based benefits such as GST/HST credit, the Canada Child Benefit (CCB) and the Guaranteed Income Supplement

(GIS)

•

Requirements to file a return

CRA encourages this because it eliminates data inputting errors on their system•

CRA can request still○

Taxpayers who electronically file their tax returns are not required to submit any receipts or supporting docs•

Taxpayers can NETFILE their personal return if specific conditions are met•

Corporations that have annual gross revenue in excess of one million have to do electronic or get penalized •

Electronic and Other filing options

Beneficial to corporations that keep their books for financial reporting purposes in a foreign currency○

Reduces the distortions that may arise under conditions of currency volatility when foreign currency results have to be translated into CAD○

An election into the foreign functional currency for tax reporting removes the need to convert financial results into Canadian dollars•

In some cases, the taxpayers would have to translate their financial results to Canadian dollars only to compute their Canadian tax liabilities•

A qualifying currency under the foreign currency election is limited to currency of the U.S, European Monetary Union, the UK, Australia, and a currency prescribed by

regulation

•

Functional currency tax reporting

PENALTIES

Penalty is 5% of the tax unpaid at the date on which the return was due to be filed•

A further penalty of 1% of the unpaid tax is levied for each complete month that the return was late up to 12 months•

Penalty equals 10% of unpaid tax plus 2% per month, up to 20 months ○

A higher penalty is for a taxpayer that violated once already in any of the three preceding years.•

Failure to file return

Only applies if the unreported income is over $500○

A penalty of the lesser of 10% of the income that a taxpayer has failed to report and 50% of the understated unpaid tax is imposed if there had been a previous failure

to report in the preceding three years

•

No penalty will apply where the more severe penalty for false statement or omission has been applied or if its over 3 years ago•

Failure to report an amount of income

Knowingly or under circumstances amounting to gross negligence under-report income•

A penalty equal to the greater of $100 and 50% of the difference in tax liability (increased tax liability x 50%)•

"gross negligence" means to include errors which amount to little more than careless omissions•

This provision would be applied to amounts excluded because of an honest dispute as to their taxability•

False statement or omission

This is to decide to treat it as a failure to report or false statement/omission•

On the first failure to report income, the first penalty would not apply so the CRA could impose the penalty for false statement or omission•

On repeated failure within 3 years, CRA may have a choice to pick•

Interplay of penalty provisions

A penalty of 50% of the interest, charged on late or underpaid instalment payments, in excess of the greater of $1000 or 25% of the interest calculated as if no

instalments had been paid

•

Penalty for late or deficient instalments

The penalty is directed to tax professionals, appraisers, and valuators and promoters of tax shelters•

First amount penalty applies where a "false statement" is made in the course of "planning activity" or "valuation activity". It is the greater of $1,000 and

the total of the person's "gross entitlement" at the time the notice of assessment of penalty is sent to the person

Second amount is $1,000, which applies in the case of a false statement in a situation that falls outside of "planning activity" and "valuation activity", or if

there's no gross entitlement either

Planner's penalty- a penalty that is imposed when the third-party person is involved in the making of, or causes another person to make a statement that the

person knowns, or would reasonably be expected to know but for circumstances amounting to "culpable conduct" is a false statement or omission that may be

used by another person for tax purposes

○

The greater of $1,000 and 50% of the amount of tax sought to be avoided, or the amount of excess refund sought to be obtained. The upper limit is

$100,000 plus the fee charged by the preparer.

See flow chart on page 850.

Preparer's penalty- a penalty that is imposed on a third-party person involved in the making of a false statement or omission statement to, or by or on behalf of,

another person. The person knows or reasonably expected to know but for circumstances amounting to "culpable conduct", is a false statement or omission

that may be used for tax purposes by or on behalf of the other person.

○

Two penalties are imposed•

Civil penalties for misrepresentation of a third party

Example problem 14-1

The taxpayer only have to pay the tax owing plus interest○

If the taxpayer makes a voluntary disclosure to correct inaccurate or incomplete information or to disclose previously unreported information, CRA can waive or

cancel penalties

•

Circumstances beyond the taxpayer's or employer's control such as natural disaster○

Actions of the Department such as processing delays, errors in CRA materials, errors in CRA advice, processing errors or CRA delays in providing information○

To facilitate collection when there is an inability to pay or where a reasonable repayment arrangement is not possible due to the heavy interest charges○

Waive interest and penalties by CRA in other occasions:•

CRA power to waive or cancel interest and penalties

A person is liable for a fine of $1,000 to $25,000 or both the fine and imprisonment for up to 12 months on summary conviction for failing to file a return as and when

required

•

A person convicted under this is not liable to pay a penalty under specified sections of the Act unless that penalty was assessed before he or she was charged under

this section

•

Making a false statement in a return○

Destroying books and records○

Falsifying books and records○

Wilfully attempting to evade compliance with the acts○

Conspiring to commit any of the above four offences○

On summary conviction, there is a fine of between 50% and 200% of tax sought to be evaded or both the fine and imprisonment for up to two years for:•

Criminal offences

Following is a summary of the payment deadline•

Individuals April 30

Corporations 2 months after year end

CCPC claiming small business deduction with taxable income under the business limit in the previous year 3 months after year end

Trusts Due date for trust return

•

Payment and interest

Individuals

Instalment threshold

5% + 1% x 12 = 17% max

10% + 2% x 20= 50% max

10% of the unreported income •

50% of understated tax liability •

Repeated offender to not report income. Lesser of

$100•

50% of increased tax liability •

Greater of:

$1,000•

25% of interest calculated as if no instalments were made•

50% of interest charged on greater of:

$1,000•

The gross entitlement •

Planner's penalty. The greater of

$1,000•

50% of tax on unreported income•

Upper limit is $100,000 + gross entitlement •

Preparer's penalty. The Great of

Did the third party know? No (Yes --> penalty)•

Would the third party be reasonably expected to know? Yes. (No --> no penalty)•

Did the third party rely in good faith on information provided by anther person? No (Yes --> no penalty)•

Did the third party exhibit culpable conduct? Yes (No --> no penalty)•

Path leading to penalty:

Error delays

Processing error

CRA fuck ups.

Chapter 14

January 5, 2018 3:31 PM

AFM 362 Page 1

Document Summary

Corporations- within six months after the end of the taxation year (their fiscal year) Individuals- on or before april 30th of the next year. Unless individual or spouse carried on a business then june 15th of the following year. Deceased individuals - if died after oct and before april 30 or june 15 then must be the later of: The usual filing date (april 30 or june 15) If dead outside of the time limit, the usual filing date apply. Trusts or estates - within 90 days after the end of the taxation year. Individuals must file only if one of the following applies: A balance of tax is owing for the year. A capital property has been disposed of in the year. A non-resident individual has a taxable capital gain (e. g. , claimed a capital gains reserve in the previous year) The individual"s home buyer plan (hbp) balance or lifelong learning plan (llp) is a positive amount.