AFM481 Lecture 9: chapter 2.5

28 Jun 2018

School

Department

Course

Professor

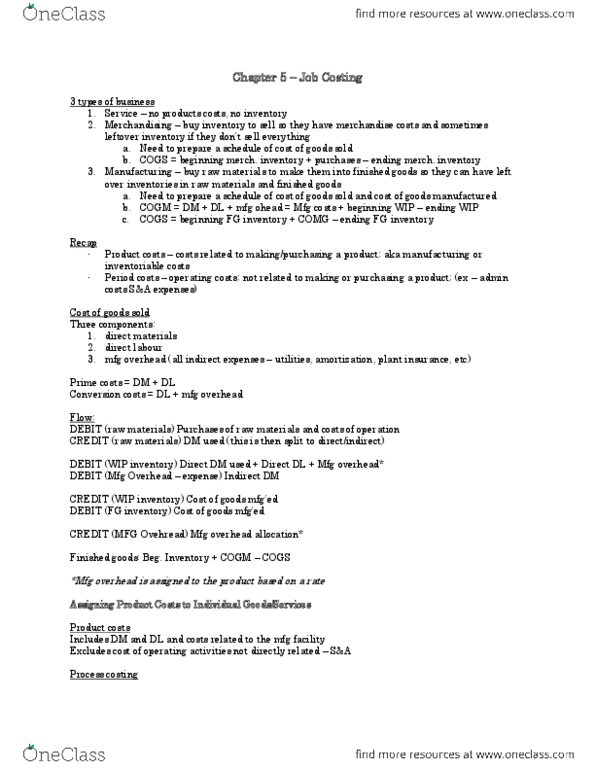

Only hold finished goods inventory (referred to as merchandise inventory)○

Merchandising sector companies purchase finished goods•

No equivalent to either cost of sales or COGS○

Service sector companies no inventory •

Are all costs of a product that are considered as assets on B/S when they are incurred•

Become COGS on the statement of comprehensive income when the product is sold•

The COGS includes all three of the manufacturing costs•

Inventoriable costs arise only for companies in the manufacturing sector•

COS includes purchasing costs of the goods, incoming freight, insurance, and handling costs ○

For merchandising sector companies, inventoriable costs are usually called cost of sales (COS)•

Typical costs classified as direct/indirect and variable/fixed for a service sector company such as

mortgage would be

•

Inventoriable costs

Are all costs in the statement of comprehensive income other than cost of goods sold•

There is not sufficient evidence to conclude that any future benefit will arise from incurring these

costs, they are not considered an asset

•

e.g. labour costs of sales floor personnel, advertising, distribution, and customer-service

costs

○

For merchandising sector companies, period costs are all costs excluded from COS •

For service sector companies, all costs are period costs•

Period costs

See page 47•

Illustrating the flow of inventoriable costs: a manufacturing-sector example

AFM 481 Page 9

Document Summary

Only hold finished goods inventory (referred to as merchandise inventory) No equivalent to either cost of sales or cogs. Are all costs of a product that are considered as assets on b/s when they are incurred. Become cogs on the statement of comprehensive income when the product is sold. The cogs includes all three of the manufacturing costs. Inventoriable costs arise only for companies in the manufacturing sector. For merchandising sector companies, inventoriable costs are usually called cost of sales (cos) Cos includes purchasing costs of the goods, incoming freight, insurance, and handling costs. Typical costs classified as direct/indirect and variable/fixed for a service sector company such as mortgage would be. Are all costs in the statement of comprehensive income other than cost of goods sold. There is not sufficient evidence to conclude that any future benefit will arise from incurring these costs, they are not considered an asset.