ECON100 Lecture Notes - Lecture 18: Potential Output, Aggregate Supply, Aggregate Demand

23 Jun 2016

School

Department

Course

Professor

Document Summary

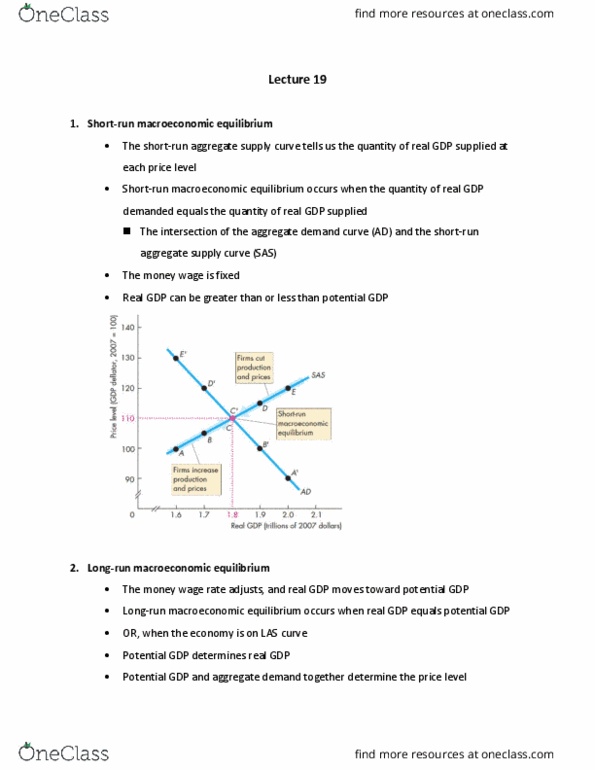

Households become optimistic and expect strong future economic growth. Increase in price level -> households buy less g&s. Movement along the curve (change in price level) Major trading partners in the world go into recession. Short run macroeconomic equilibrium occurs when the quantity of real gdp demanded equals the quantity of real gdp supplied at the point of intersection of the ad curve and the sas curve. Suppose price level is above current equilibrium. Excess supply of goods and services -> produce less until its at equilibrium. Long run macroeconomic equilibrium occurs when real gdp equals potential. Gdp when economy is on its las curve. Long run equilibrium occurs at intersection of the ad and las curve. Assume economy is below full employment equilibrium. In the long run, money wage falls until the sas curve passes through the long run equilibrium point. Suppose instead that the economy is initially at an above full employment equilibrium.