COMM 294 Lecture Notes - Lecture 11: Earnings Before Interest And Taxes, Contribution Margin, Net Income

Document Summary

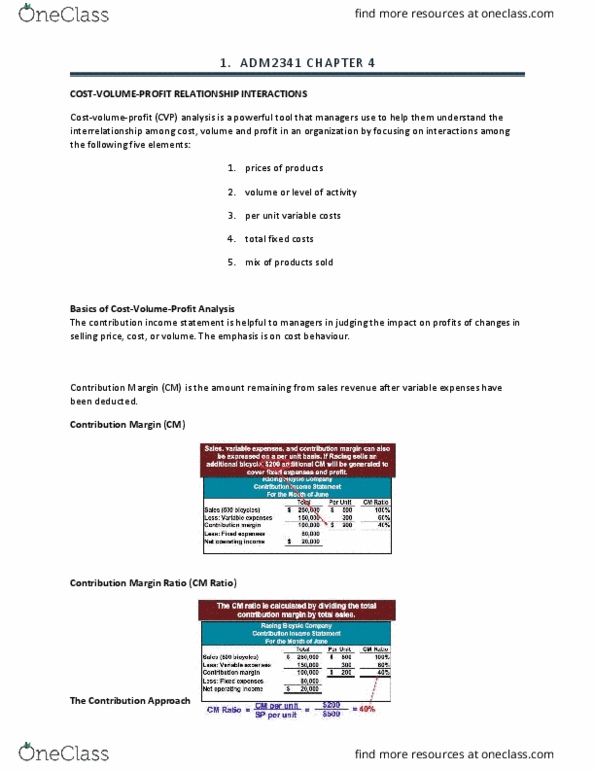

Comm 294, cost- volume- profit (cvp) analysis. The contribution income statement is helpful to managers in judging the impact on profits of changes in selling price, cost, or volume. Contribution margin (cm) is the amount remaining from sales revenue after variable expenses have been deducted. )total cm vs. unit cm vs. cm ratio: total contribution margin (tcm) vs, unit contribution margin (ucm) vs, contribution margin ratio. 500300usp : unit selling price200100%60%40%= cm / revenues = cm ratio= 200 / 500 = 40%tcmucmucm: extra pro t for producing & selling one more unitcm ratio = ucm / usp = tcm / total salesthe contribution approach. If rbc sells 400 units in a month, it will be operating at the break- even point. If rbc sells one more bike (401 bikes), net operating income will increase by . We do not need to prepare an income statement to estimate profits at a particular sales volume.