COMM 294 Lecture Notes - Lecture 23: Transfer Pricing, Contribution Margin, Market Price

Document Summary

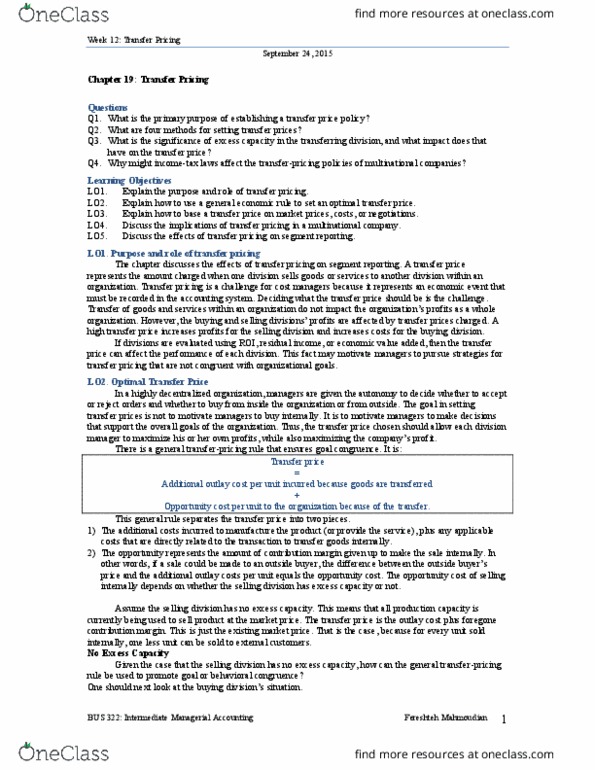

Reporting for control (chapter 11): transfer pricing. The transfer price shifts profits between divisions. But it does not (directly) affect the profit of the company as a whole. Transfer pricing why is it important: transfer prices affect the basis for each segment"s performance evaluation (profit, costs, revenues). This affects both the supplying division and the buying division. Can alter the incentives of the divisional managers. Three methods will be discussed: Use the market price of similar goods traded on an external market to set your internal transfer price. Advantages: avoids need for negotiations, forces supplying division to be competitive, does not penalize buying division. Transfer price is based on cost of producing the product. Advantages: commonly used in practice, easily understood and convenient to use. Disadvantages: may obscure and lead to inefficiencies, distinction between fixed and variable costs are blurred. Selling division and buying division negotiate a transfer price. Upper limit is determined by the buying division.