COMM 353 Lecture Notes - Lecture 40: Taxation In Canada, Dividend Tax, Corporate Tax

Document Summary

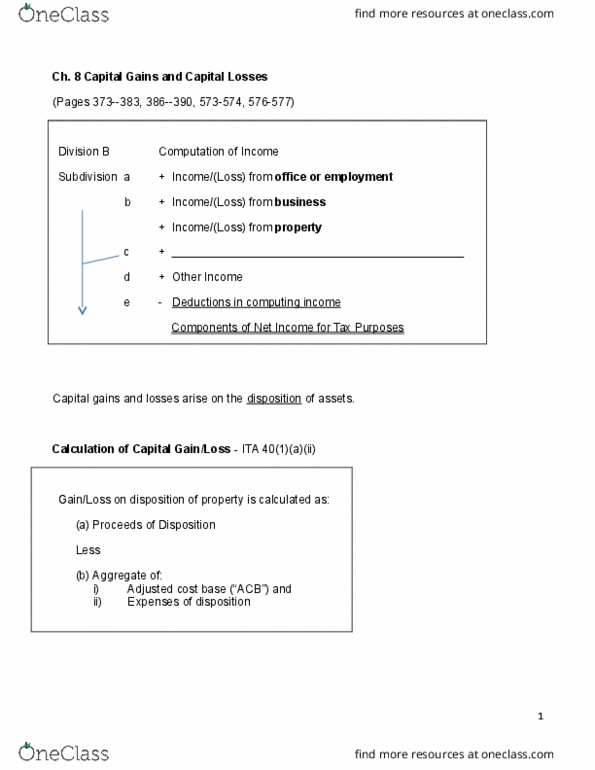

7 income or loss from property (relevant textbook pages are 325-330, 332-337, 810-814) + taxable capital gains allowable capital losses. Dividends from a corporation resident in canada. States that when interest is received or receivable, it must be included in income to the extent that the interest has not been included previously by the accrual method. For corporations, partnerships, trusts use the accrual method. Similar to accounting (exception is interest income on bonds that have been purchased at a premium or discount) For individuals modified version of accrual accounting. Accrue interest on each anniversary date of an investment contract. Anniversary date day before the date that is one year after the date of issue of the security, and every successive one year interval. Eg) if debt issued on sept 1, 20x1, then anniversary date would be aug. 31, 20x2, aug. 31, 20x3, etc.