BUSI 1915U Lecture Notes - Lecture 8: Contribution Margin, Net Income, Variable Cost

Document Summary

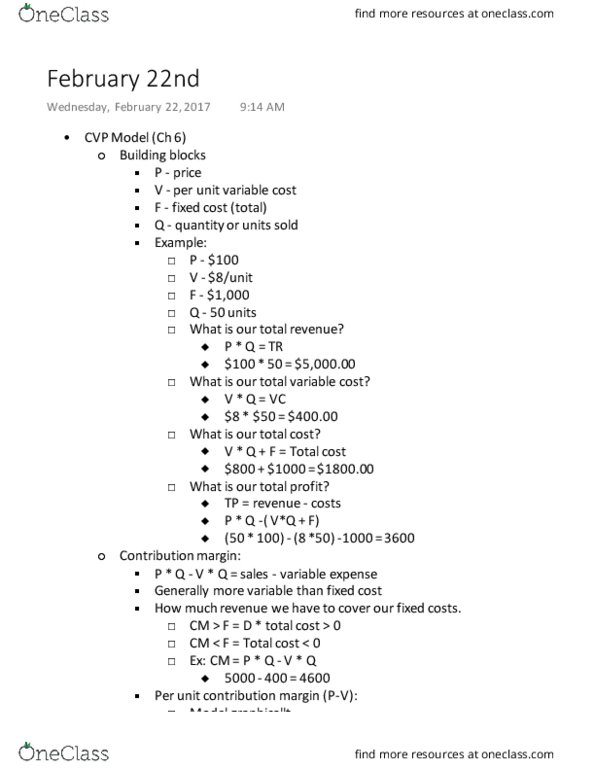

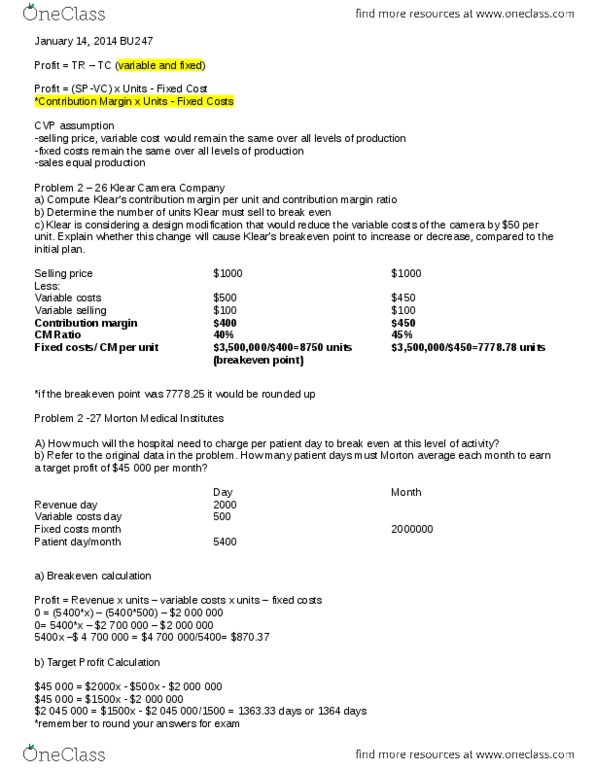

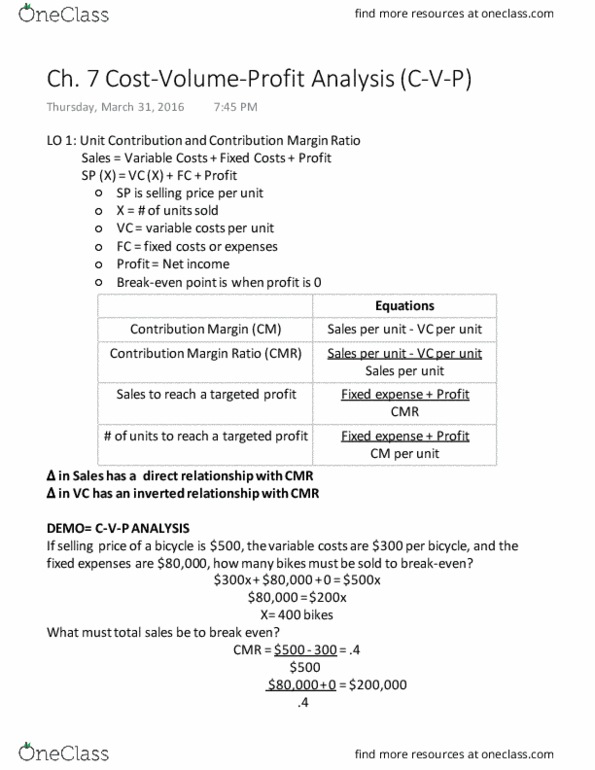

A technique for estimating firm"s operating profit at any sales volume, given the firm"s costs. A valuable tool in evaluating the potential effects of decisions on profitability. Break-even analysis: looks at break even point - the point at which neither a profit or loss is made. Costs: all costs that must be taken into account including fixed costs and the variable costs. Volume: the level of output of a machine, department, or organization, or the quantity of sales. Revenue: the gross income generated by the sale of a product. Profit: the net income obtained by subtracting all costs from the revenue. Fixed costs: do not change if sales increase or decrease. Fixed costs per unit of output decrease as volume increases because the total cost is spread out over more units. Examples: rent, property taxes, supervision and management salaries, etc. Variable costs: change in direct proportion to sales volume.