BUSI 2160U Lecture Notes - Lecture 6: Accounts Payable, Inventory Turnover, Capital Structure

Document Summary

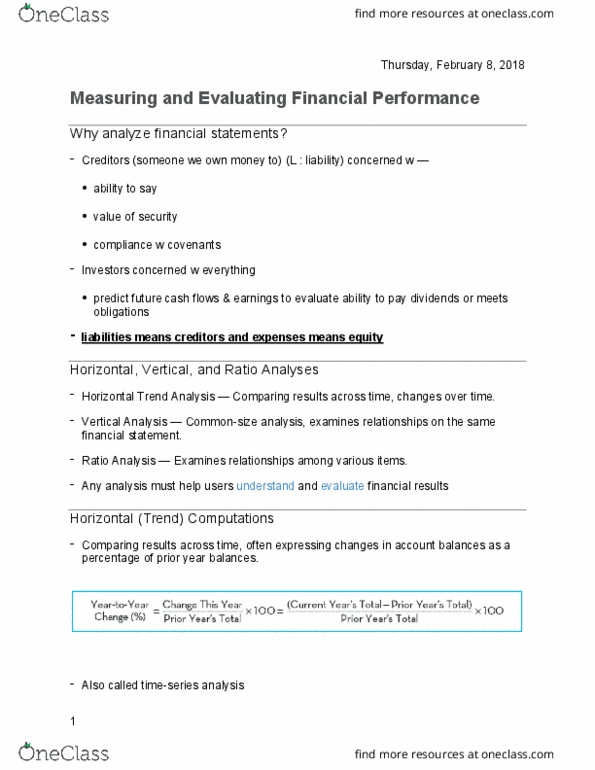

Users include: creditors, equity investors, other stakeholders. How financial statements are used to help make decisions: evaluate profitability, project future earnings, assess and project cash flows, determine compliance with covenants, assess the risk of the entity, evaluate performance. Creditors concerned: ability to pay, value of security, compliance with covenants investors concerned with everything, predict future cash flows and earnings to evaluate ability to pay dividends or meet obligations. Not part of ordinary operations unusual. Gains and losses on disposal of capital assets and investments. Earning = cash from operations + accruals. Ratio of r&d expense to sales = (cid:3019)&(cid:3005) (cid:3006)(cid:3051)(cid:3043)(cid:3032)(cid:3041)(cid:3046)(cid:3032) (cid:3020)(cid:3028)(cid:3039)(cid:3032)(cid:3046) Interpreting raw numbers can be challenging: difficult to compare different entities, difficult to compare different years. Eliminate impact of size of financial statement numbers by restating as proportions. Solution: vertical analysis common size financial stmts, horizontal analysis trend financial stmts. = (cid:3045)(cid:3042)(cid:3046)(cid:3046) (cid:3014)(cid:3028)(cid:3045)(cid:3034)(cid:3041) (cid:3030)(cid:3042)(cid:3046)(cid:3047) (cid:3042)(cid:3033) (cid:3046)(cid:3028)(cid:3039)(cid:3032)(cid:3046) (cid:2869)(cid:2868)(cid:2868)% (cid:3020)(cid:3028)(cid:3039)(cid:3032)(cid:3046) Gross margin % = (cid:3020)(cid:3028)(cid:3039)(cid:3032)(cid:3046) (cid:3030)(cid:3042)(cid:3046)(cid:3047) (cid:3042)(cid:3033) (cid:3046)(cid:3028)(cid:3039)(cid:3032)(cid:3046) (cid:2869)(cid:2868)(cid:2868)% (cid:3020)(cid:3028)(cid:3039)(cid:3032)(cid:3046)