MGM222H5 Lecture Notes - Lecture 7: Sunk Costs, Skimmed Milk, Condensed Milk

At least two will be on final exam

6 situations

1) Buy or keep (equipment)

2) Add or drop (product/ segment)

3) Make or buy/ outsource (part)

4) Special orders

5) Joint costs – sell / produce further

6) Constraints resources

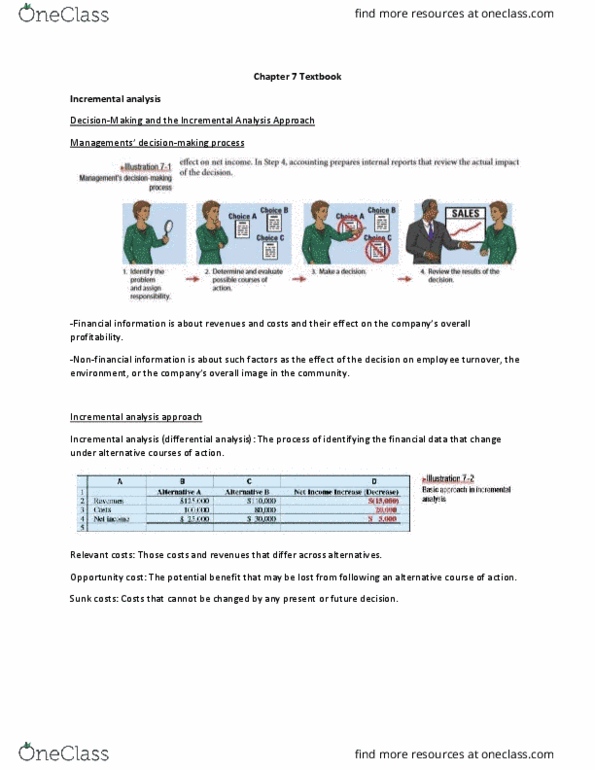

Management’s decision-making process

1) Issue

2) Alternatives

3) Choose alternative

4) Implement/ feedback

Considers both financial and non-financial info

- Financial:

o Revenues and costs

- Non-financial:

o Effect of decision on employee turnover

o Environment

o Overall image

- How incremental analysis works

-

find more resources at oneclass.com

find more resources at oneclass.com

- Need to analyze & state which one is better

Relevant costs

- Avoidable costs

o Differ for each situation

o Future costs = relevant

- Unavoidable costs = non-relevant

- VC change

- FC do not change

o May develop

Opportunity cost

- Benefits forgiven if you select one alternative over another

Sunk cost

- Will not be changed or avoided by future decisions

Book value of an asset

- Not relevant, sunk cost

o But residual value?

A general rule:

- Future revenues and costs which differ are always relevant

Special order

- Should not be accepted if not operated at full capacity

- Ex)

o 100,000 / 80% = 125,000 units

o Selling it at $11 when TC = $12; so we should not accept this

o Or: 11 Selling Price – 8 VC = 3 unit *2000 = $6000 net income (Accept)

▪ How will that affect customers?

Make or buy ex)

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

At least two will be on final exam. 6 situations: buy or keep (equipment, add or drop (product/ segment, make or buy/ outsource (part, special orders, joint costs sell / produce further, constraints resources. Non-financial: effect of decision on employee turnover, environment, overall image. Need to analyze & state which one is better. Avoidable costs: differ for each situation, future costs = relevant. Benefits forgiven if you select one alternative over another. Will not be changed or avoided by future decisions. Future revenues and costs which differ are always relevant. Should not be accepted if not operated at full capacity. Things to consider: v moh costs that will be saved by the decision, f moh costs that will be eliminated, purchase price, opportunity costs. Based on costs: based on analysis of costs under both alternatives, purchasing adds ,000 to cost of switches. Thus, the ,000 lost income is an additional cost of making the switches.