MGM101H5 Lecture Notes - Initial Public Offering, Unsecured Debt, Stock Certificate

25

MGM101H5 Full Course Notes

Verified Note

25 documents

Document Summary

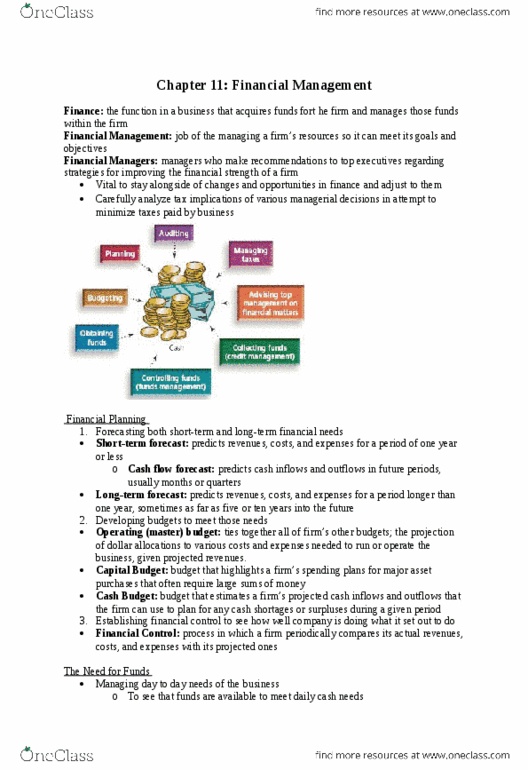

Finance: the function in a business that acquires funds fort he firm and manages those funds within the firm. Financial management: job of the managing a firm"s resources so it can meet its goals and objectives. Financial managers: managers who make recommendations to top executives regarding strategies for improving the financial strength of a firm. Vital to stay alongside of changes and opportunities in finance and adjust to them. Carefully analyze tax implications of various managerial decisions in attempt to minimize taxes paid by business. Financial planning: forecasting both short-term and long-term financial needs. Short-term forecast: predicts revenues, costs, and expenses for a period of one year or less: cash flow forecast: predicts cash inflows and outflows in future periods, usually months or quarters. Long-term forecast: predicts revenues, costs, and expenses for a period longer than one year, sometimes as far as five or ten years into the future: developing budgets to meet those needs.