MGT120H5 Lecture Notes - Cash Flow Statement, Inventory Turnover, Perpetual Inventory

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

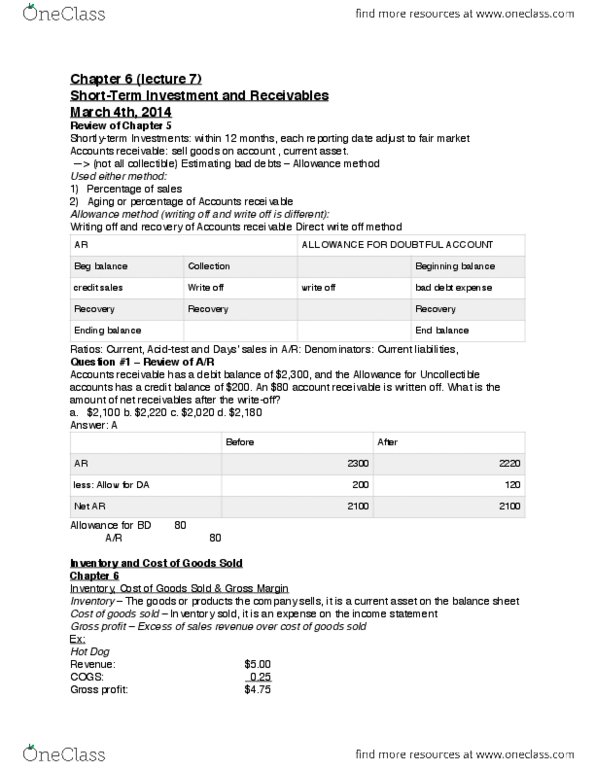

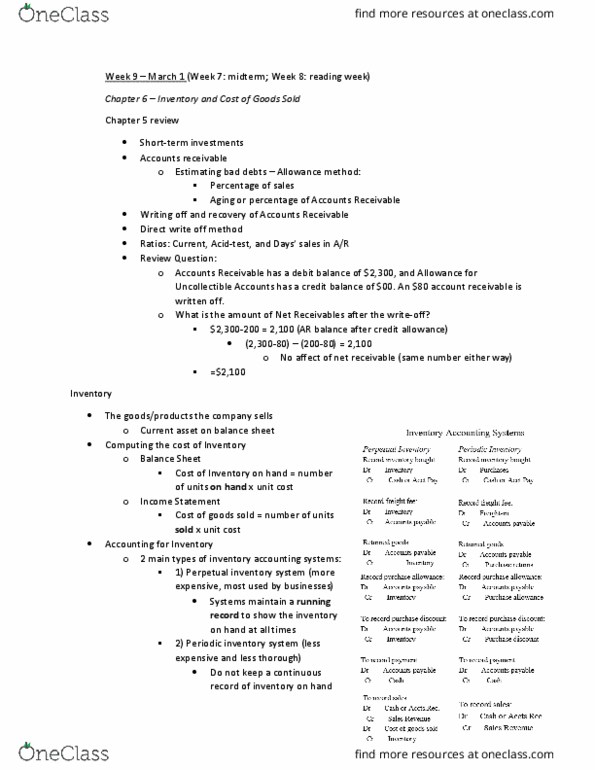

Short term investments: intend to sell within 12 months, each reporting date adjust to fair market value. Accounts receivable: aging or percentage of accounts receivable. Ratios: current, acid test, and days" sales in a/r. Question 1 review of a/r: accounts receivable has a debit balance of 2300, and the allowance for uncollectible accounts has a credit balance of . Solution: net recievables: a/r allowance for doubtful accounts. Before: a/r : 2300, less: allowance for doubtful accounts : 200, net a/r : 2100. Less: allowance for doubtful accounts: 120, net a/r 2100: 2,100, 2,220, 2,020, 2,180. Cr a/r 80 (5,000x13) + (4,000 x 12) = 113,000. Abc ltd had a 24,000 beginning inventory and a 26,000 ending inventory. Net sales were 160,000; purchases, ,000; purchase returns and allowances, 5000 and freight in , . Cost of goods sold for the period is.