MGT120H5 Lecture Notes - Book Value, Capital Expenditure, Sept

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

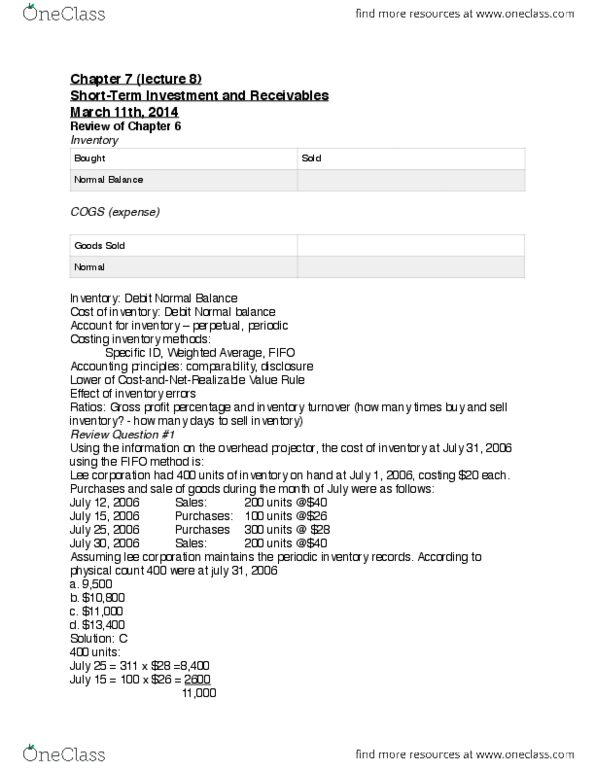

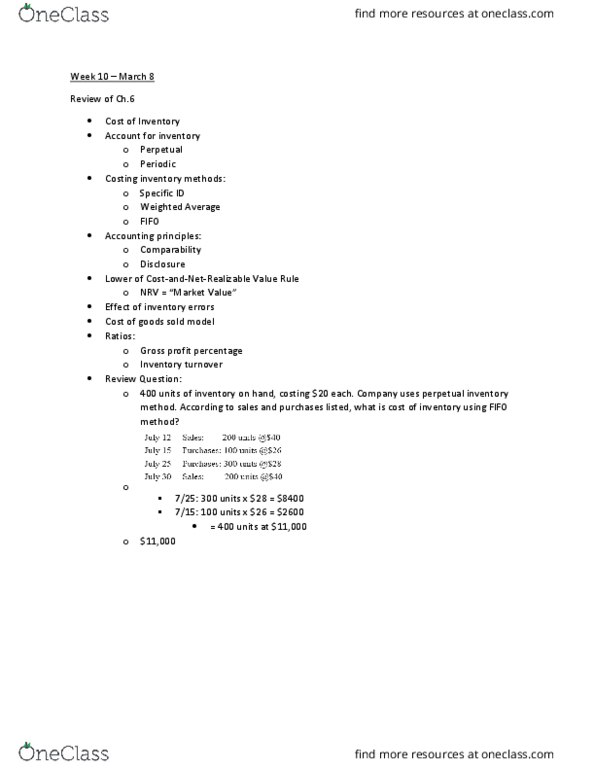

Accounting principles: comparability being able to compare previous years with this year"s financial statements. Disclosure: notes any discrepancies or additional information. Lower of cost and net realizable value rule : before prepare financial statements compare actual cost with net realizable value and choose the lower of the 2 amounts. Effect of inventory errors: get carried over to the next fiscal year. Lee corporation had 400 units of inventory on hand at july 12006, costing 20 each. Purchases and sales of goods during the month of july were as follows. According to physical count 400 units were on hand at july 31 2006. *answer multiple choice question 1 with this question* Using the information on the overhead projector, the cost of inventory at july 31, 2006 using the fifo method is: Land and building were bought for a total of 458000. The market value for the land was 175000 and. 315250: 9500, 10800, 11000, 13400, 175000, 160000, 175000, 169750.