ACCT 3600 Lecture Notes - Lecture 1: Financial Audit, Financial Statement, Accounting

2 Sep 2015

School

Department

Course

Professor

Document Summary

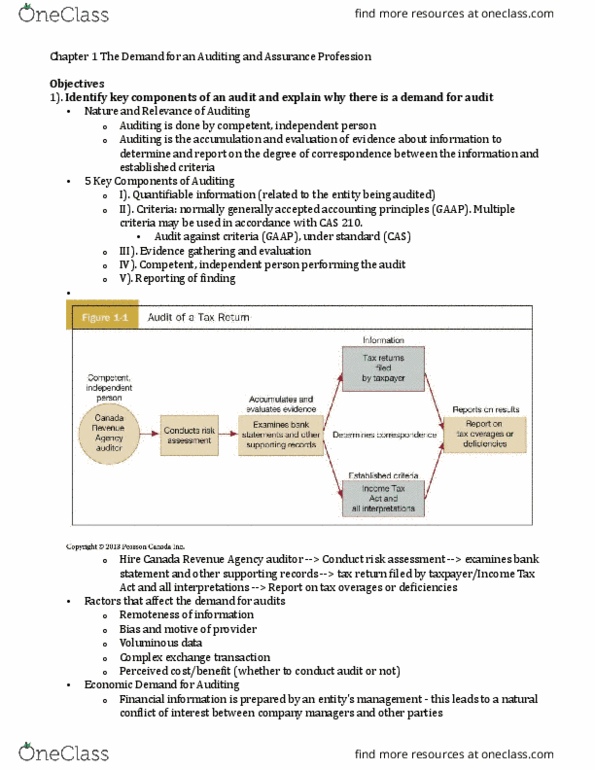

Learning objectives: identify the components of an audit and explain why there is a demand for audits. Differentiate accounting from auditing: distinguish audit engagements from other assurance and non assurance services, describe the different types of accountants and what they do. Auditing is the accumulation and evaluation of evidence about information to determine and report on the degree of correspondence between the information and established criteria. Auditing should be done by a competent and independent person text p. 5. Information information such as that contained in financial statements. 70-360 and management"s assertions that the financial statements information is presented fairly. Generally accepted accounting principles (gaap) in canada now there are a number of different types of gaap ifrs and aspe being the two most widely used. To prepare a report - re financial statements information the auditor"s. Re financial statements information achieved through the financial statement audit. Auditing: quantifiable information (related to entity, criteria: normally generally accepted accounting principles (gaap).