BU127 Lecture Notes - Lecture 16: Promissory Note, Cash Flow, Interest Expense

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

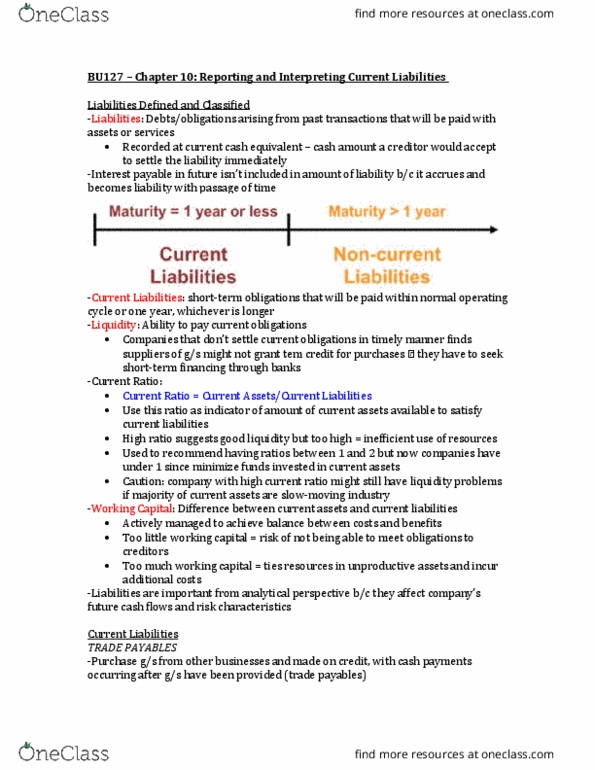

Working capital = current assets current liabilities. Changes in working capital accounts are important to managers and analysts because they have a direct impact on cash flows from operating activities reported on the statement of cash flows. Liquidity is the ability to pay current obligations. Warranty provision: start balance of 773m, paid out expenses of 224m, end balance of. 725m warranty expense = start paid out end = 773 224 725 = -176 = 176m. Company buys new capital on jan 1, 2017, signed a note agreeing to pay ,000 on dec 31, 2018 the market interest rate for this note is 12% Pv = / (1. 12)^2 = ,440 journal entry for example above on jan 1, 2017: delivery trucks (+a) Journal entry on dec 31, 2017 ( * 0. 12 = ) Journal entries on dec 31, 2018 ( * 0. 12 = ) Annuities: equal payments are made each period, the payments and interest accumulate over time.