BU227 Lecture : Chapter 8 Reporting and Interpreting Cost of Sales and Inventory

Document Summary

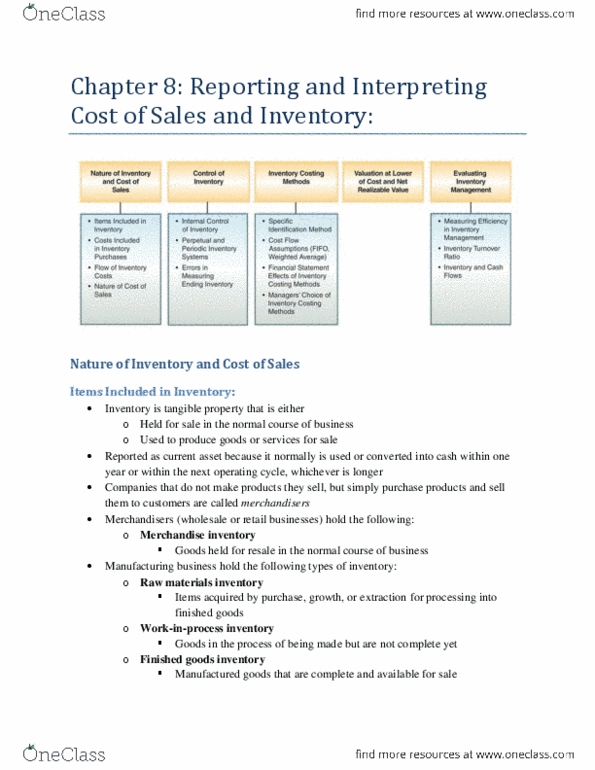

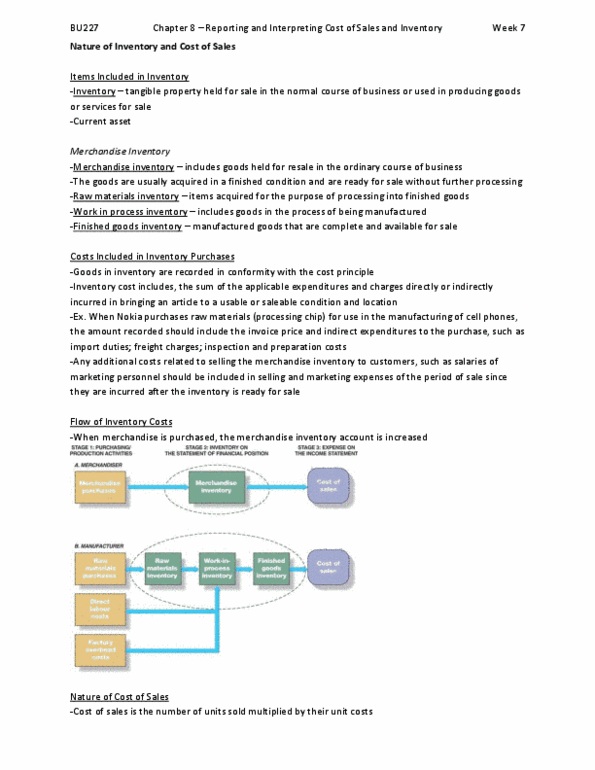

Chapter 8: reporting and interpreting cost of sales and inventory. Merchandisers: companies that do not manufacture the products they sell, but simply purchase those products then sell them to customers. Items acquired by purchase, growth (food), or extraction (natural resources) for processing into finished goods. Included in raw materials inventory until used, at which point they become part of work-in-process inventory. Manufactured goods that are complete and available for sale. Cost principle: the sum of applicable expenditures and charges directly/indirectly incurred in bringing an article to a usable or saleable condition and location (not current value) Include the invoice price and indirect expenditures related to the purchase, such as import duties; freight charges, inspection and preparation costs (not a lot; sometimes just recorded as expense) Company should cease accumulating purchase costs when the raw materials are either ready for use or when the merchandise inventory is ready for shipment.