1. A cost pool is :

A. a collection of homogeneous cost to be assigned.

B. almost always the combined result of decision made bydifferent responsibility center manager.

C. The primary function of a responsibility accountingsystem.

D. the amount of cost that has been allocated say, 10% to a userdepartment.

E. The tool used to allocate cost dollars to userdepartments.

2.Variable costs are those costs that:

A. vary (in total ) inversely with changes in activity.

B. vary (in totals) directly with in activity.

C. remain constant (in total) as activity changes.

D. Decrease on a per unit basis as activity increase.

E. Increase on a per unit basis as activity increases.

3. When comparing EOQ and JIT inventory system, which of thefollowing statement is false?

A. The EOQ approach takes the viewpoint that some inventory isnecessary.

B. The EOQ system assumes a constant order quantity.

C. JIT argues that inventory investments should beminimized.

D. The EOQ system focuse on acquistion and holding costs.

E. JIT argues that safety stocks are necessary to reduce theprobability of a stock shortage.

4. Procust costing in manufacturing firm is the process of:

A. Accumulating the company 's period costs

B. Allocating costs among the firm departments.

C. Placing a value on the company's fixed assets.

D. Assigning cost to the firm's inventory.

E. Assinging costs to the comapny's managers.

5.Decentralized firms can delegate authority by structuring anorganization into responsibility centers. Which of the followingorganizational segments is most like a totally independent,standalone business where managers are expected to "make it on theown?

A. Cost center

B. Revenue Center

C. Profit Center

D. Investment center

E. Contribution center

6. Costs that are expensed when incurred are called:

A. Product costs

B. Direct Costs

C. Inventoriable Cost

D. Period Cost

E. Indirect costs

7. A budget serves as a benchmark against which:

A. Actual result can be compared

B. Allocated results can be compared

C. actual result be inconsequential

D. Alloated results become inconsequential.

E. Cash balances can be compared to expense totals.

8. Activity based costing system.

A. use a single volume based cost driver.

B. Assign overhead to product based on the products' relativeusage of direct labor.

C. often reveal products that were under or over costed bytraditional costing.

D. Typically use fewer cost driver than more traditional costingsystem.

E . Have a tendency to distort product costs/

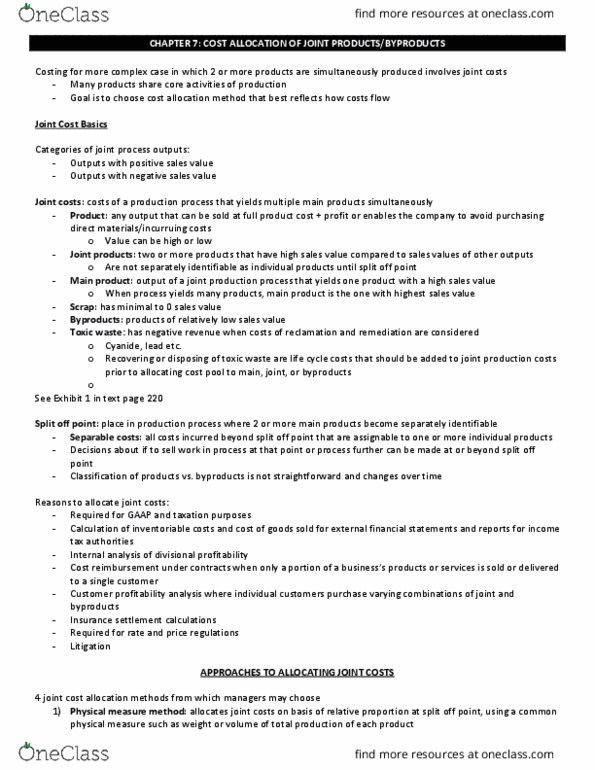

9.The point in a joint production process where each individualproduct becomes separately identifiable is commonly called the:

A. Decision point

B. Separation point

C. Individual product point

D. Split-off point

E. Joint product point.

10.The RIO calculation will indicate:

A. the percentage of each sale dollar that is invested inassets.

B. The sale dollars generated from each dollar of income.

C.How effectively a company used its invested capital

D. the invested capital generated from each dollar of income

E. the overall quality of the company's earnings.