ACCT-241 Lecture Notes - Lecture 9: Earnings Before Interest And Taxes, Liability Insurance

21 Aug 2018

School

Department

Course

Professor

Document Summary

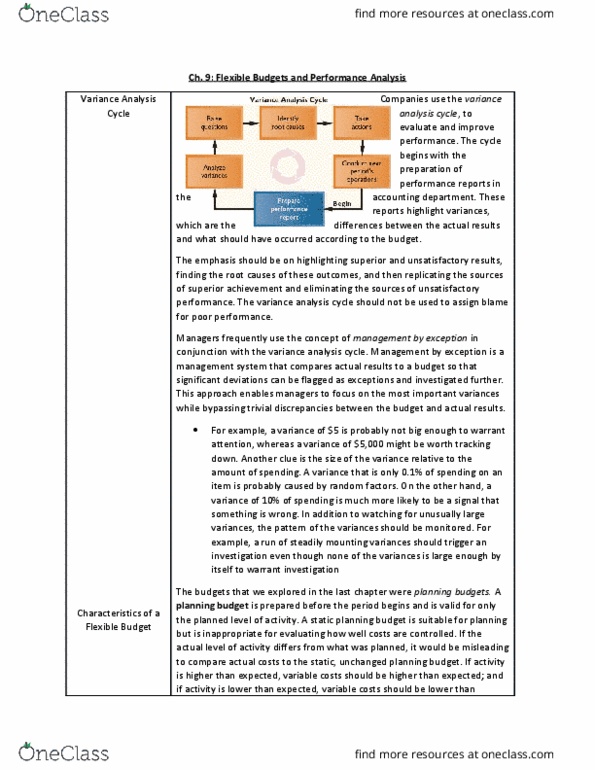

Companies use the variance analysis cycle,as illustrated in exhibit 9 1,to evaluate and improve performance. The cycle begins with the preparation of performance reports in the accounting department. These reports highlight variances, which are the differences between the actual results and what should have occurred according to the budget. The significant variances are investigated so that their root causes can be either replicated or eliminated. Then, next period"s operations are carried out and the cycle begins again with the preparation of a new performance report for the latest period. The emphasis should be on highlighting superior and unsatisfactory results, finding the root causes of these outcomes, and then replicating the sources of superior achievement and eliminating the sources of unsatisfactory performance. The variance analysis cycle should not be used to assign blame for poor performance. The budgets that we explored in the last chapter were planning budgets.