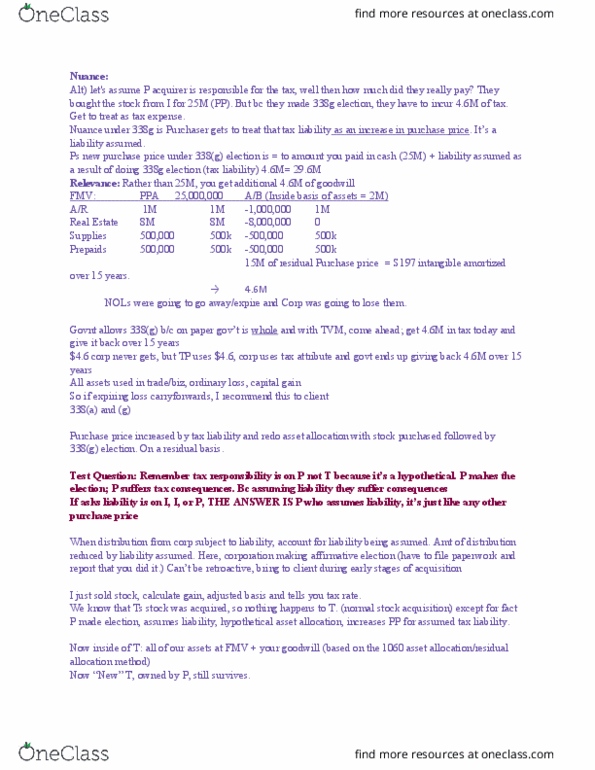

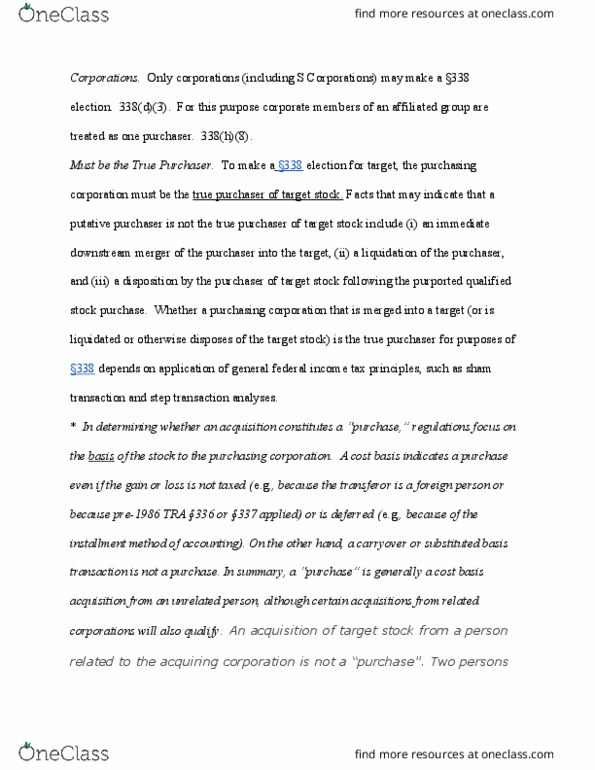

TAX 9866 Lecture Notes - Lecture 3: Target Corporation, S Corporation

Get access

Related Documents

Related Questions

Helen Bowers, owner of Helen's Fashion Designs, is planning to request a line of credit from her bank. She has estimated the following sales forecasts for the firm for parts of 2016 and 2017:

| may 2016 | $186,000 |

| june | 186,000 |

| july | 372,000 |

| august | 540,000 |

| september | 720,000 |

| october | 360,000 |

| november | 360,000 |

| december | 90,000 |

| january 2017 | 180,000 |

Estimates regarding payments obtained from the credit department are as follows: collected within the month of sale, 10%; collected the month following the sale, 75%; collected the second month following the sale, 15%. Payments for labor and raw materials are made the month after these services were provided. Here are the estimated costs of labor plus raw materials:

| may 2016 | $90,000 |

| June | 90,000 |

| july | 126,000 |

| august | 881,000 |

| september | 307,000 |

| october | 234,000 |

| november | 162,000 |

| december | 90,000 |

a.General and administrative salaries are approximately $26,000 a month. Lease payments under long-term leases are $9,000 a month. Depreciation charges are $36,000 a month. Miscellaneous expenses are $2,600 a month. Income tax payments of $63,000 are due in September and December. A progress payment of $180,000 on a new design studio must be paid in October. Cash on hand on July 1 will be $132,000, and a minimum cash balance of $90,000 should be maintained throughout the cash budget period.

Prepare a monthly cash budget for the last 6 months of 2016. If no entry required, enter "0". Use minus sign to enter losses, loans outstanding or any other negative amounts.

| may | june | july | august | september | october | november | december | january | |||||||||

| collecions and purchases worksheet | |||||||||||||||||

| sales (gross) | $ | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||

| collections | |||||||||||||||||

| during month of sale | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||

| during 1st month after sale | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||

| during 2nd month after sale | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||

| total collections | $ | $ | $ | $ | $ | $ | |||||||||||

| purchases | |||||||||||||||||

| labor and raw materials | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||

| payments for labor and raw materials | $ | $ | $ | $ | $ | $ | $ | ||||||||||

| cash gain or loss for month | |||||||||||||||||

| collections | $ | $ | $ | $ | $ | $ | |||||||||||

| payments for labor and raw materials | $ | $ | $ | $ | $ | $ | |||||||||||

| general and administrative salaries | $ | $ | $ | $ | $ | $ | |||||||||||

| lease payments | $ | $ | $ | $ | $ | $ | |||||||||||

| miscellaneous expenses | $ | $ | $ | $ | $ | $ | |||||||||||

| income tax payments | $ | $ | $ | $ | $ | $ | |||||||||||

| design studio payment | $ | $ | $ | $ | $ | $ | |||||||||||

| total payments | $ | $ | $ | $ | $ | $ | |||||||||||

| net cash gain (loss) during month | $ | $ | $ | $ | $ | $ | |||||||||||

| Loan Requirement or cash surplus | |||||||||||||||||

| cash at start of month | $ | $ | $ | $ | $ | $ | |||||||||||

| cumulative cash | $ | $ | $ | $ | $ | $ | |||||||||||

| target cash balance | $ | $ | $ | $ | $ | $ | |||||||||||

| cumulative surplus cash or loans outstanding to maintain $90,000 target cash balance | |||||||||||||||||

| $ | $ | $ | $ | $ | $ |

b. Prepare monthly estimates of the required financing or excess funds - that is, the amount of money Bowers will need to borrow or will have available to invest. Round your answers to the nearest dollar. Enter loans outstanding with minus sign.

| July | $ |

| august | $ |

| september | $ |

| october | $ |

| november | $ |

| december | $ |

During the current year, Marlene, Nancy and Olive formed a new SCorporation. Solely in exchange for stock, Marlene and Nancycontributed appreciated property, while Olive contributed services.The exchanges of Marlene and Nancy will be nontaxable if:

Olive receives 30% of the stock | ||

Olive receives 80% of the stock | ||

Olive receives 15% of the stock | ||

Marlene and Nancy together receive 50% of the stock |

In June of 2018, Alice acquired heronly machine for $30,000 to use in her business. The machine isclassified as 5-year property. Aliceâs maximum depreciation(including bonus) on the machine this year is:

$30,000 | ||

$12,000 | ||

$6,000 | ||

$18,000 |

Cactus Corporation, an S Corporation, had accumulated earningsand profits of $200,000 at the beginning of the tax year. Tex andShirley each own 50% of the stock. During the current year Cactushad $100,000 of ordinary income and distributed $10,000 to Tex and$10,000 to Shirley. What is Tex's taxable income for the currentyear?

$10,000 | ||

$0 | ||

$100,000 | ||

$50,000 |

Bristol Corporation was formed as an S Corporation on January 1,2014 and elected S corporation status at that date. Bristol has hadthe same 25 shareholders throughout its existence and has one classof stock. Bristol's S election will terminate if it:

10% of the shareholders vote to revoke the election | ||

to purchase 10 shares | ||

Allows a variation in the voting rights of the stock | ||

Increases the number of shareholders to 125 |

On February 10, 2018, Ace Corporation, a new calendar yearcorporation, elected S corporation status and all shareholdersconsented to the election. There was no change in its shareholdersduring the current year. Ace met all eligibility requirements foran S corporation during the preelection portion of the year. Whatis the earliest date on which Ace can be recognized as an Scorporation?

February 10, 2018 | ||

January 1, 2019 | ||

February 10, 2019 | ||

January 1, 2018 |

In March of 2017 Frederick acquired an passenger automobile for$45,000 and used the automobile 85% for business. Themaximum depreciation deduction for 2017 is:

$3,160 | ||

$11,160 | ||

$8,928 | ||

$9,486 |

In August of 2017, Joseph acquires andplaces into services business equipment costing $300,000. Theequipment is classified as 5-year recovery property. No otheracquisitions are made during the year. Joseph elects to expense themaximum amount under Sec. 179. Josephâs total deductions for theyear are

$60,000 | ||

$500,000 | ||

$100,000 | ||

$300,000 |

For the current tax year, VBN, an S Corporation distributes$100,000 to its sole shareholder, Raymond. His basis in the stockwas $140,000 before the distribution. VBN had once been a regular CCorporation and had remaining accumulated earnings and profits(E&P) from those years of $70,000. However, VBN has no balancein its accumulated adjustment account. How should the distributionof $100,000 be handled?

$100,000 as a taxable distribution

$70,000 as a taxable dividend, and $30,000 has a non taxablereturn of capital

$50,000 as a taxable dividend, and $100,000 as a non taxablereturn of capital

$70,000 as a taxable dividend; and $30,000 as a capital gain

Stahl, an individual who owns 100% of Talon, an S corporation,had a basis of $50,000 at the first of the year. During the yearTalon reported the following: Ordinary Loss of $10,000; Municipalinterest income of $8,000, Long term capital gain of $4,000; andLong term capital loss of $9,000. What was Stahl's basis in Talonat year end?

$56,000 | ||

$65,000 | ||

$53,000 | ||

$43,000 |

Gross Receipts of $70,000; Tax Exempt Interest Income of $4,000;Dividends of $10,000; Supplies Expense of $3,000; and UtilitiesExpense of $1,500. What amount is the S Corporation's ordinarytaxable income?

$75,500 | ||

$79,500 | ||

$70,000 | ||

$65,500 |

Bob and Sam each owned 50% of Lostalot, an S Corporation. Bob'sbasis is $30,000 and Sam's basis is $15,000. The corporation hasoperating loss for the current year of $50,000. Howmuch loss can each shareholder deduct in the current year assumingthey materially participate in the business:

Bob: $25,000; Sam: $15,000 | ||

Bob: $0; Sam: $0 | ||

Bob: $25,000; Sam: $25,000 | ||

Bob: $30,000; Sam: $15,000 |

Terra Corporation, a calendar-yeartaxpayer, purchases and places into service in 2017 machinery witha 7-year life that cost $650,000. The mid-quarter convention doesnot apply. Terraâs taxable income for the year before the Sec. 179deduction is $700,000. What is Terraâs total maximum depreciationdeduction related to this property?

$585,718 | ||

$521,345 | ||

$92,885 | ||

$500,000 |

Identify which of the following statements is false.

The PTI (previously taxed income) represents the balance ofundistributed net income which were already taxed. | ||

The AAA balance can be negative, but the shareholder's basis inthe S corporation stock cannot be less than zero. | ||

Tax exempt income increase the AAA and the basis of the Scorporation stock. | ||

| An S Corporation may or may not have accumulated Earnings andProfits Elaine owns an unincorporated manufacturing business. In 2017,she purchases and places in service $600,000 of qualifying fiveyear equipment for use in her business. Her taxable income from thebusiness before any section 179 deduction is $100,000. Which of thefollowing statements is true? |

Elaine cannot deduct any Section 179 deduction for 2017 | ||||||||||||||

Elaine can deduct $100,000 as a Section 179 deduction in 2017with a $400,000 carryover to next year. | ||||||||||||||

Elaine can deduct $100,000 as a Section 179 deduction in 2017with a $500,000 carryover to the next year | ||||||||||||||

| Elaine can deduct $500,000 as a section 179 deduction in2017 Charles, an individual, owned 100% of the Alpha, an Scorporation. At the first of the year, Charles' basis in Alpha was$25,000. In the current year, Alpha realized ordinary income of$1,000; and a long term capital gain of $3,000. Alpha distributed$25,000 to Charles at the end of the year. What amount of the$25,000 is taxable to Charles?

|

Note:

This question has been answered totally from 1-8 questions in previuos requested, the only part ( need to answer ) I need to help me with that to have completed the calculations, provide a brief, two- to four-sentence rationale for how these calculations can be used in analyzing the financial position of a company and why they are important. Your rationale should explain what information the ratio provides to the reader and how the reader may use that information.

I will repeat tyoing the question for make it clearing .

Analysis of Financial Statements

Balance Sheets

EXHIBITS: INPUT DATA (XYZ)

Table 1 Balance Sheets

| Assets | 2013E | 2012 | 2011 |

| cash | $ 85,632 | $7,282 | $57,600 |

| Acount Receivable | 878,000 | 632,160 | 351,200 |

| Inventories | 1,716,480 | 1,287,360 | 715,200 |

| Total current assets | $2,680,112 | $1,926,802 | $ 1,124,000 |

| Gross fixed assets | 1,197,160 | 1,202,950 | 491,000 |

| Less: accumulated depreciation | 380,120 | 263,160 | 146,200 |

| Net fixed assets | $ 817,040 | $ 939,790 | $ 344,800 |

| Total assets | $3,497,152 | $2,866,592 | $ 1,468,800 |

| Liabilities and equity | |||

| Accounts payable | $ 436,800 | $ 524,160 | $ 145,600 |

| Notes payable | 300,000 | 636,808 | 200,000 |

| Accruals | 408,000 | 489,600 | 136,000 |

| Total current liabilities | $1,144,800 | $1,650,568 | $ 481,600 |

| Long term bonds | 400,000 | 723,432 | 323,432 |

| Total debt | $1,544,800 | $2,374,000 | $ 805,032 |

| Common stock (100,000 shares) | 1,721,176 | 460,000 | 460,000 |

| Retained earnings | 231,176 | 32,592 | 203,768 |

| Total common equity | $1,952,352 | $ 492,592 | $ 663,768 |

| Total liabilities and equity | $3,497,152 | $2,866,592 | $ 1,468,800 |

Analysis of Financial Statements

Income Statements

Table 2

Income Statements

| 2013E | 2012 | 2011 | |

| Sales | $7,035,600 | $6,034,000 | $ 3,432,000 |

| Cost of goods sold | 5,875,992 | 5,528,000 | 2,864,000 |

| Other expenses | 550,000 | 519,988 | 358,672 |

| Total operating exp. excl. depreciation and amortization | $6,425,992 | $6,047,988 | $ 3,222,672 |

| EBITDA | $ 609,608 | $(13,988) | $ 209,328 |

| Depreciation and amortization | 116,960 | 116,960 | 18,900 |

| Earnings before interest and taxes (EBIT) | $492,648 | $(130,948) | $190,428 |

| Interest expense | 70,008 | 136,012 | 43,828 |

| Earnings before taxes (EBT) | $ 422,640 | $ (266,960) | $ 146,600 |

| Taxes (40%) | 169,056 | (106,784) | 58,640 |

| Net Income | $ 253,584 | $ (160,176) | $ 87,960 |

| Earnings per share (EPS) | $ 1.014 | $ (1.602) | $ 0.880 |

| Dividends per share (DPS) | $ 0.220 | $ 0.110 | $ 0.220 |

| Book value per share (BVPS) | $ 7.809 | $ 4.926 | $ 6.638 |

| Stock price | $ 12.17 | $ 2.25 | $ 8.50 |

| Shares outstanding | 250,000 | 100,000 | 100,000 |

| Tax rate | 40.00% | 40.00% | 40.00% |

| Lease payments | $ 40,000 | $ 40,000 | $ 40,000 |

| Sinking fund payments | 0 | 0 | 0 |

Analysis of Financial Statements

Ratio Analysis

| 2013E | 2012 | 2011 | Industry Average | |

| Current ratio | * | 1.2 | 2.3 | 2.7 |

| Quick ratio | * | 0.4 | 0.8 | 1.0 |

| Inventory turnover | * | 4.7 | 4.8 | 6.1 |

| Days sales outstanding (DSO) | * | 38.2 | 37.4 | 32.0 |

| Fixed assets turnover | * | 6.4 | 10.0 | 7.0 |

| Total assets turnover | * | 2.1 | 2.3 | 2.6 |

| Debt-to- assets ratio | * | 82.8% | 54.8% | 50.0% |

| Times interest earned (TIE) | * | -1.0 | 4.3 | 6.2 |

| Operating margin | * | -2.2% | 5.6% | 7.3% |

| Profit margin | * | -2.7% | 2.6% | 3.5% |

| Basic earning power (BEP) | * | -4.6% | 13.0% | 19.1% |

| Return on assets(ROA) | * | -5.6% | 6.0% | 9.1% |

| Return on equity (ROE) | * | -32.5% | 13.3% | 18.2% |

| Price/earnings (P/E) | * | -1.4 | 9.7 | 14.2 |

| Market/book (M/B) | * | 0.5 | 1.3 | 2.4 |

| Book value per share (BVPS) | * | $4.93 | $6.64 | n.a. |

Requiremnts:

1. Calculate XYZâs 2013 current and quick ratios based on the projected balance sheet and income statement data.

2. Calculate the 2013 inventory turnover, days sales outstanding (DSO), fixed assets turnover, and total assets turnover.

3. Calculate the 2013 debt-to-assets and times-interest-earned ratios.

4. Calculate the 2013 operating margin, profit margin, basic earning power (BEP), return on assets (ROA), and return on equity (ROE).

5. Calculate the 2013 price/earnings ratio, and market/book ratio.

6. Use the extended DuPont equation to provide a summary and overview of XYZâs financial condition as projected for 2013.

7. Use the following simplified 2013 balance sheet to show, in general terms, how an improvement in the DSO would tend to affect the stock price. For example, if the company could improve its collection procedures and thereby lower its DSO from 45.6 days to the 32-day industry average without affecting sales, how would that change âripple throughâ the financial statements (shown in thousands below) and influence the stock price?

Accounts receivable $878 Debt $1,545

Other current assets 1,802

Net fixed assets 817 Equity 1,952

Total assets $3,497 Liabilities plus equity $3,497

First, we need to calculate XYZâs daily sales.

Daily sales = Sales / 365

Daily sales = $7,035,600 / 365

Daily sales = $19,275.62

Target A/R = Daily sales à Target DSO

Target A/R = $19,276 Ã 32

Target A/R = $616,820

Freed-up cash = old A/R â new A/R

Freed-up cash = $878,000 â $616,820

Freed-up cash = $261,180

Note : All questions from 1-8 has been answered, but the only part I need help with to write the analysis or to provide a brief, two- to four-sentence rationale for how these calculations can be used in analyzing the financial position of a company and why they are important.