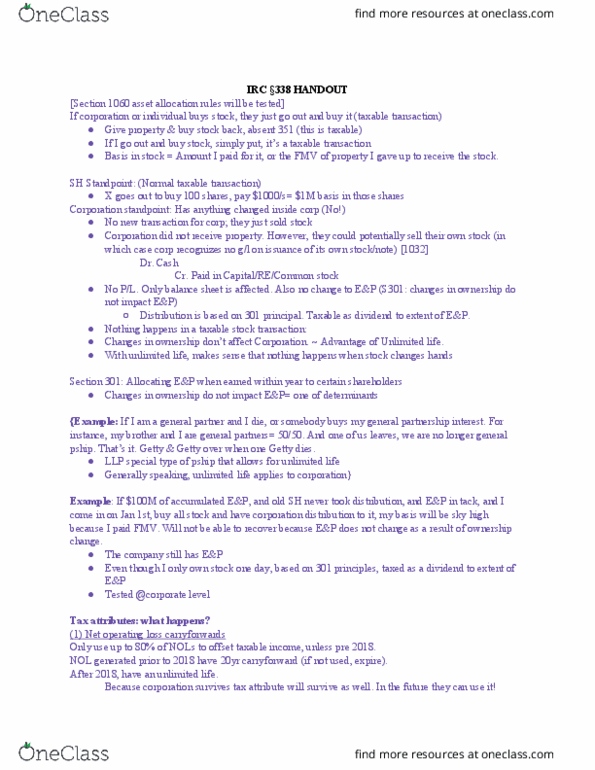

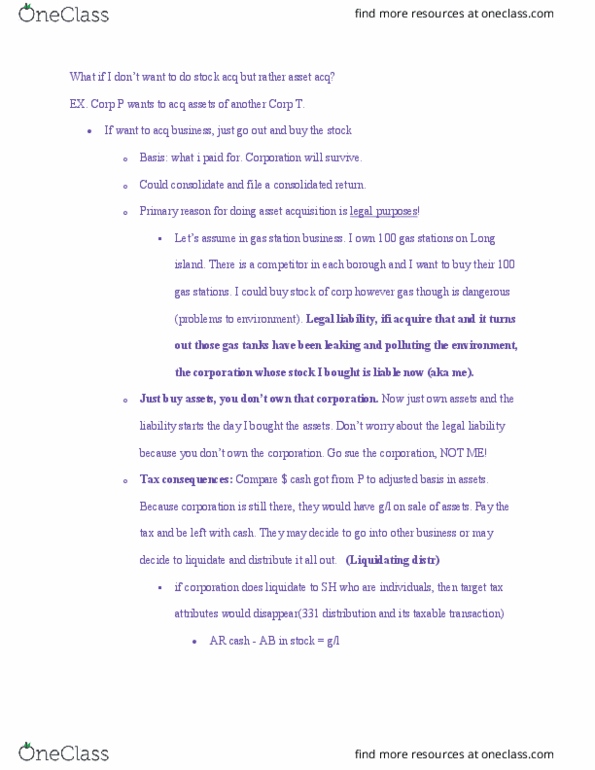

Jack and Jill Uphill are the shareholders of JJ Art, Inc., an S corporation which conducts business as an art gallery in Miami Beach, FL. The corporation was formed in 1986, and the corporation has always been an S corporation. JJ Art, Inc. also owns the real estate used in the business. Jill inherited the land from her grandfather upon his death in 1985, and she transferred the property to the corporation solely in exchange for stock of the corporation in a nonrecognition transaction to which Code Section 351 applied. Her grandfather had purchased the real estate for $10,000 many years earlier. The fair market value of the property as finally determined for federal estate tax purposes upon her grandfatherâs death was $300,000. The real property was then unencumbered and remains so today. The real estate consists of the land and a free standing building with a total fair market value of $4,000,000. The corporationâs total basis in the real estate (land and building) on the date of distribution is $20,000. On January 20, 2017, JJ Art, Inc. adopted a plan of complete liquidation, and on February 20, JJ Art., Inc. distributed the real estate pro rata to its two shareholders. How much gain or loss, if any, was realized and recognized by the corporation as a result of the distribution of the real estate to Jack and Jill?

a.0, because this is an S corporation.

b. $280,000.

c. $3,980,000.

d. 0, because this is a distribution to the individual shareholders in liquidation of the corporation.

My answer is (b) 280,000. Am I on the right track? If not can you tell me what answer you derived at and how.