TAX 9866 Lecture Notes - Lecture 13: Not I, Capital Gain, Income Tax

Document Summary

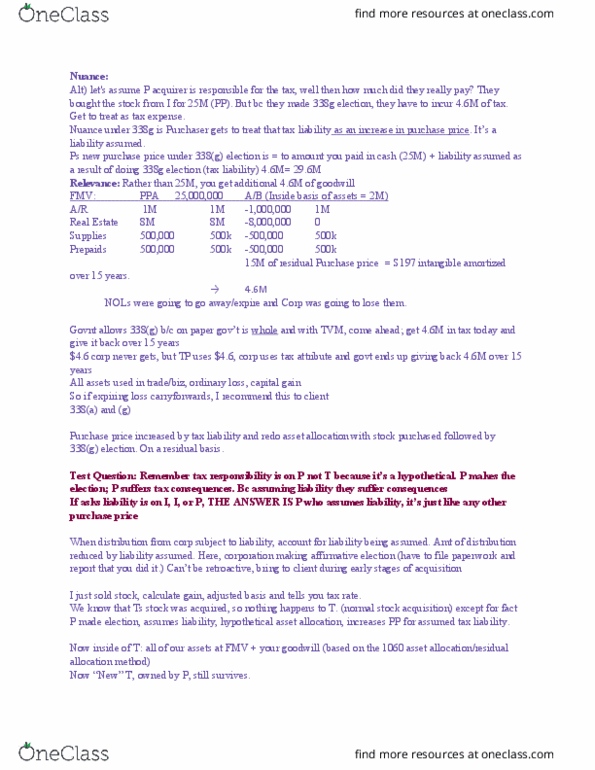

Outside basis = (what i paid for stock m) 23m disconnect. Never recover that 23m bc all u own is stock (until you sell never going to recover stock basis) unless you use asset purchase election or straight up buy assets directly. Class 2: actively traded personal property marketable securities. Class 3: assets that tp marks to market at least annually accounts receivable, mortgage receivable, Class 4: assets are stock in trade of tp (includible in inventory/ primarily for sale to customers) Class 5: all other assets not defined in classes 1-4, or 6 or 7. Class 6: all s197 intangibles, except goodwill and going concern value e. g. customer list, covenant not to compete. {4 categories of identifiable, most liquid to least} Rule: if you run out of purchase price you stop bc doing it on residual basis and then nothing goes to lower tier asset [will not ask us where it runs out]