TAX 9873 Lecture Notes - Lecture 10: Leveraged Buyout, Cash Flow

Document Summary

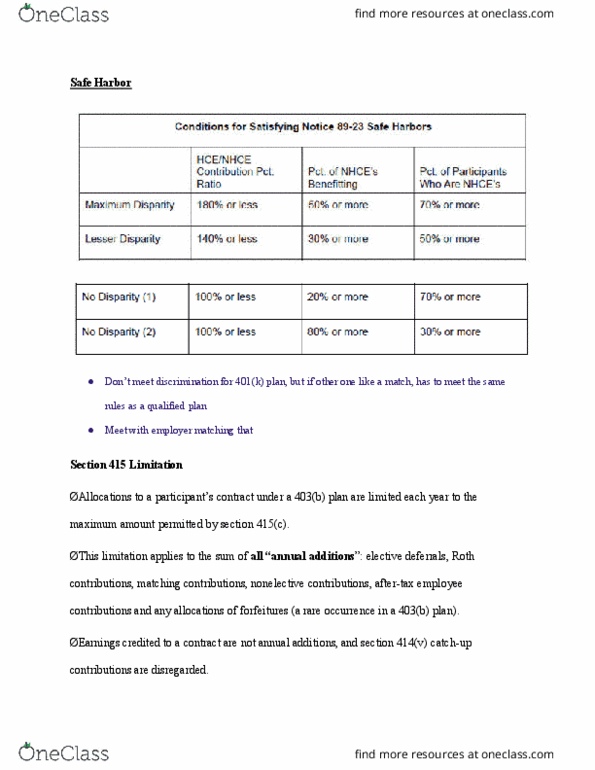

Qualified non-elective contributions as elective contributions for purposes of adp test. Matching contributions that are eligible to be treated as elective are referred to as qualified matching contributions. Qualified non-elective and qualified matching contributions may be treated as elective contributions. Distributions permitted upon plan termination must be in lump sum: death, disability, severance from employment, termination of plan, employees on temporary leave while performing services in uniform(military) attainment of age 59 or under hardship. Financial hardship: participant has an immediate and heavy financial need, distribution needed to satisfy financial need, special distrib. Payment of college/grad school for employee, spouse, child, dependent. Elected employees in top paid group that are top 20% Following can be excluded for compensation purposes: reimbursement, fringe benefit, moving exp, deferred comp, welfare benefits. Safe harbor provisions created so that its easier for plans to satisfy nondiscrimination tests. Allows owners and hce to make max salary deferral regardless of other employee contrib.