TAX 9873 Lecture Notes - Lecture 51: Tax Avoidance, The Employer, De Minimis

Document Summary

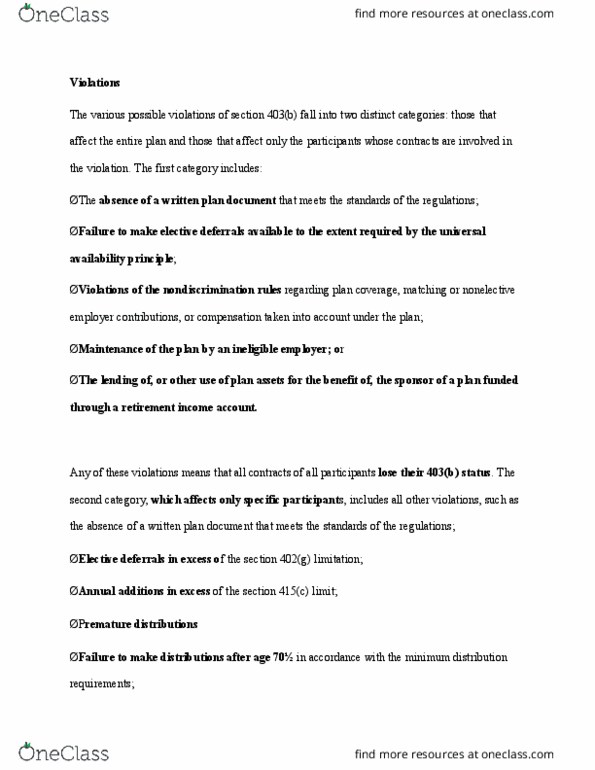

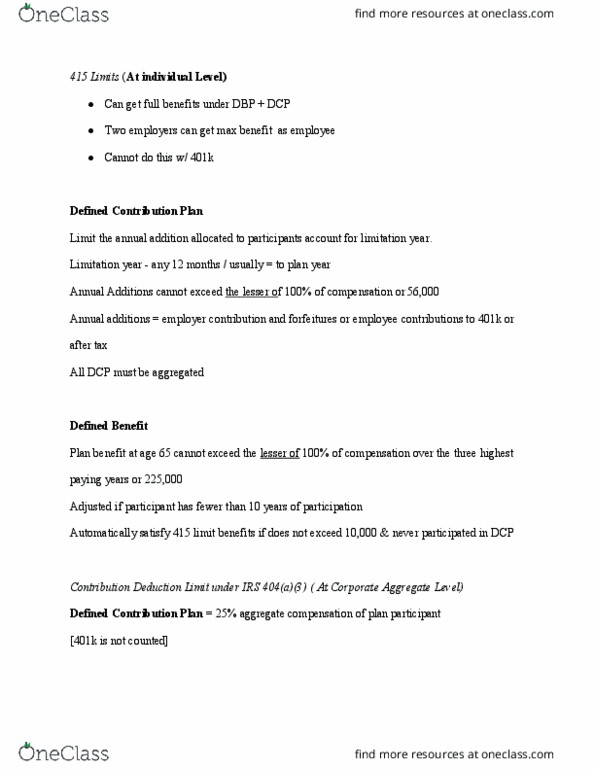

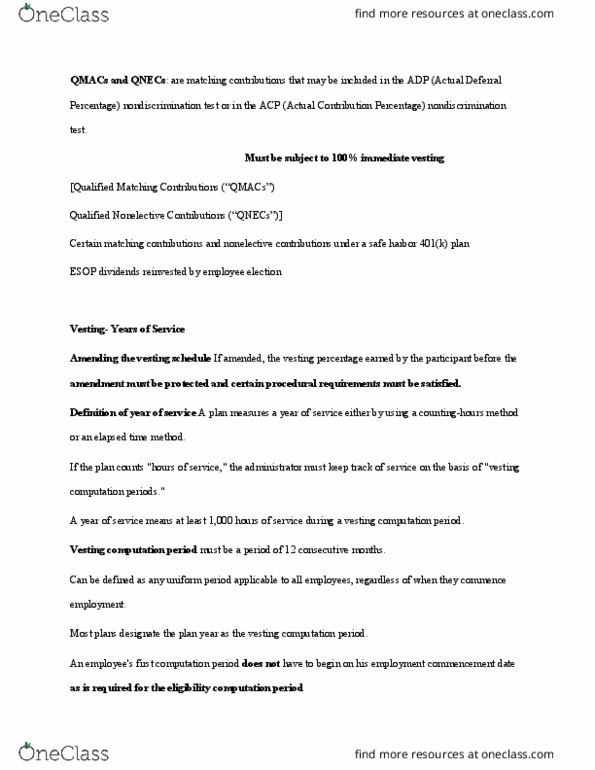

Don"t meet discrimination for 401(k) plan, but if other one like a match, has to meet the same rules as a qualified plan. Allocations to a participant"s contract under a 403(b) plan are limited each year to the maximum amount permitted by section 415(c). This limitation applies to the sum of all annual additions : elective deferrals, roth contributions, matching contributions, nonelective contributions, after-tax employee contributions and any allocations of forfeitures (a rare occurrence in a 403(b) plan). Earnings credited to a contract are not annual additions, and section 414(v) catch-up contributions are disregarded. Earnings do not determine how much can be funded. The distribution rules applicable to 403(b) plans depend on the type of contribution and the funding vehicle. Elective deferrals have one set of restrictions, very similar to those for section. Upon distribution, allow direct rollovers of distributions at the participant"s request. 10% early withdrawal penalty like a qualified plan.