UGBA 180 Lecture Notes - Lecture 9: Tax Deduction, Debt Service Coverage Ratio, Tax Rate

25 Jun 2018

School

Department

Course

Professor

Lecture 9: Investment Analysis II

Monument Office set Up

●Investor maybe 8.5M purchase

○Hold 5 years and resell

●96k sq ft

●3 current tenants w/leases expiring over next 5 years

○Base rent

○Expense stops

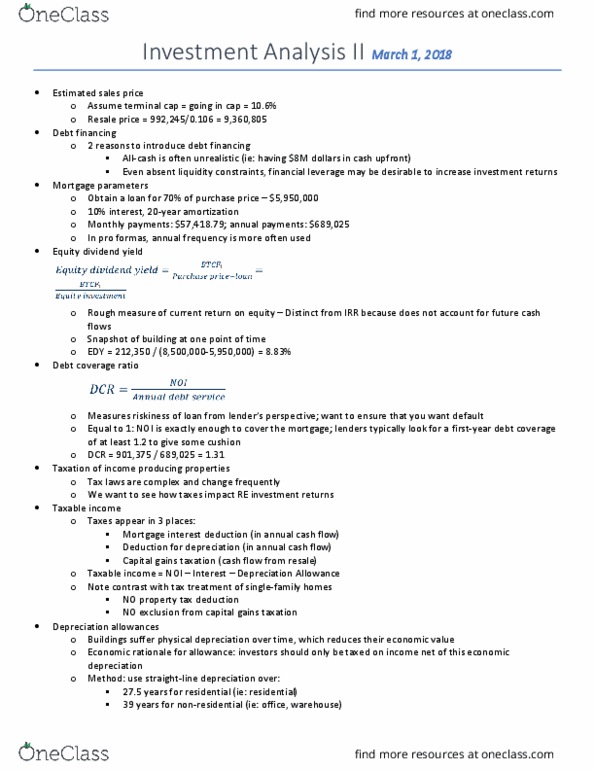

Intro Debt Financing

●So far: assuming investor pays for monument out of pocket

●2 reasons to introduce debt financing

○All cash is often unrealistic

○Even absent liquidity constraints financial leverage may be desirable to increase

investment returns

●Mortgage Parameters

○Obtain a lona for 70% of purchase price

■$5.95 M

■10% interest

■20 year amortization

■Monthly payments -> $57,418.79

■Annual payments -> $689,025

○Annual Loan Schedule

●Equity Dividend Yield

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

3 current tenants w/leases expiring over next 5 years. So far: assuming investor pays for monument out of pocket. Even absent liquidity constraints financial leverage may be desirable to increase investment returns. Obtain a lona for 70% of purchase price. Rough measure of curr return on equity. Distinct from irr bc it doesn"t account for future cash flows. Measures riskiness of lean from lender"s perspective. Lenders typically want first year debt coverage of at least 1. 2. Taxable income = noi - interest - depreciation allowance. Note contrast with tax treatment of single family homes. Buildings suffer physical depreciation over time which reduced their economic value. Economic rationale for allowance: investors should only be taxed on income net of this economic depreciation. Nonresidential buildings use straight-line depreciation over 39 years. I. e. depreciate 1/39th of the building"s basis each year. Depreciation allowances often exceed actual depreciation -> tax benefits. Can deduct an amount > amount by which building"s value has actually declined.