SMG AC 222 Lecture Notes - Lecture 1: Lean Manufacturing, Management Accounting, Indian Railways

28 Jul 2016

School

Department

Course

Professor

Document Summary

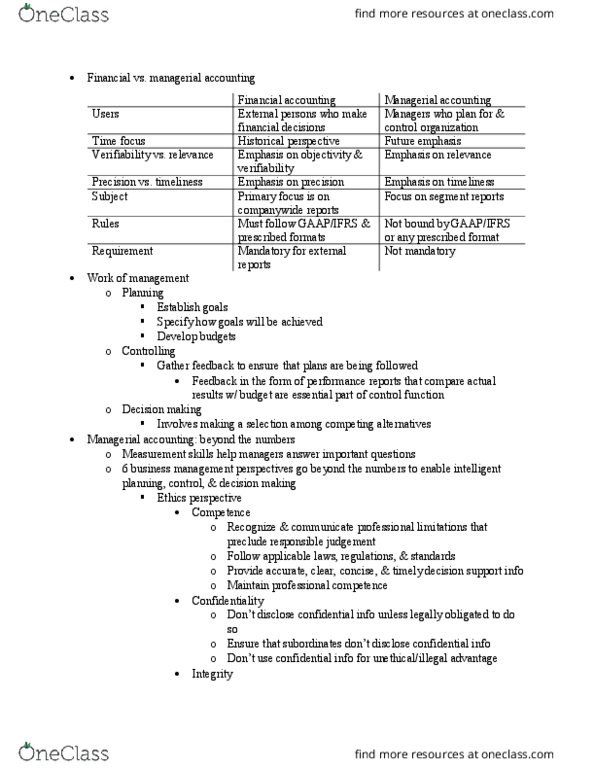

Chapter 1: differences between financial accounting and managerial accounting. Do not have to follow gaap: process of management. Planning: establish goals-specify process-develop budgets (set target goals/profit targets) Controlling: gather feedback to ensure that plans are being followed (such as performance forms to keep track the difference between expectation and actual results) Decision making: sell or not sell, purchase or manufacture, rent size, what should we sell, who are our investors: some terms. Lean manufacturing: reduce waste as much as you can. Fixed cost: not change with production amount, usually paid by month or quarter or year. Cost (graph 1) change proportionally with the increasing of producing units (graph 3) constant within relevant. Fixed cost range (easier to understand graphically) (graph 2) constant within relevant range (graph 4) decrease with the decreasing of producing units. Opportunity cost: the potential benefit that is given up when one alternative is selected over another.