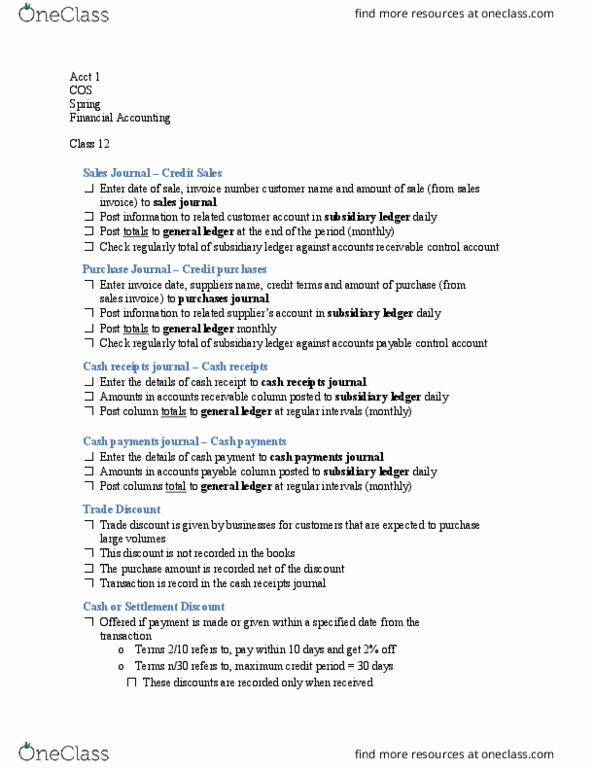

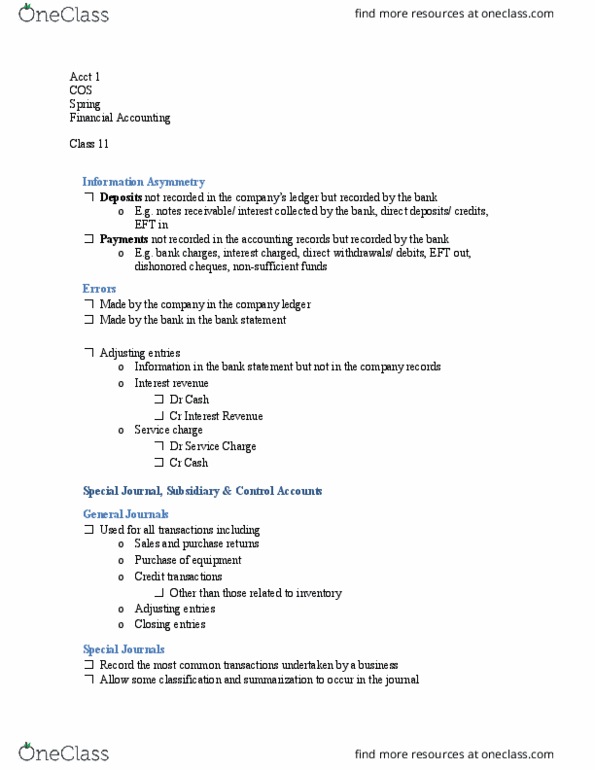

ACCT 001 Lecture Notes - Lecture 11: Accounts Receivable, Income Statement, Balance Sheet

Document Summary

Get access

Related Documents

Related Questions

Felbin Inc. is in the second quarter of its first year ofoperations, and it plans to use the allowance method to account forits receivables. The CFO of the company is evaluating threedifferent approaches to the allowance method, and the impact thateach may have on the company's financial statements. The CFOestimates sales for the year will be $4.75 million, with $4.5million on credit. The tax rate for Felbin is 30%. The CFO asks youto prepare an analysis of what the year-end journal entries mightlook like under three different assumptions. Based on youranalysis, the CFO will determine which one of the three independentapproaches to take when recording bad debts expense atyear-end.

Assumption 1: Income Statement Approach

Felbin uses the income statement approach and estimates 2% ofcredit sales will be uncollectible. In the event economicconditions worsen during the year, the CFO would revise hisuncollectible percentage to 3%.

Assumption 2: Balance Sheet Approach

Felbin uses the balance sheet approach with estimateduncollectibles of 2% of ending receivables. This will result in anestimated charge to bad debt expense of $84,200. The uncollectiblepercentage would be increased to 2.5% if economic conditionsworsen.

Assumption 3: Aging Approach

As an alternative to the basic balance sheet approach, the CFO hasdrafted an estimated aging schedule (shown below). If economicconditions worsen, the CFO believes a one percentage point increasein the uncollectible percentages would be appropriate.

Days Outstanding | A/R Amount | Estimated Percent Uncollectible | Estimated $ Uncollectible | Percent if Economy Worsens |

Less than 30 days | 1,750,000 | 1% | 17,500 | 2% |

30â60 days | 1,395,000 | 3% | 41,850 | 4% |

61â120 days | 820,000 | 5% | 41,000 | 6% |

Greater than 120 days | 245,000 | 20% | 49,000 | 21% |

Total | 149,350 |

Using the CFO's estimate of sales and accounts receivable forthe year, prepare the following proposed journal entries for theCFO to review:

A.) Assuming the Income Statement approach is used and economicconditions do not worsen, prepare the journal entry that would bemade for the year.

B.) Assuming the Income Statement approach is used and economicconditions worsen, provide the journal entry that would be made forthe year.

C.) Assuming the Balance Sheet approach is used and economicconditions worsen, provide the journal entry that would be made forthe year.

D.) Assume the aging method is used. What is the expected chargeto bad debt expense under the assumption that economic conditionsworsen?

2) On January 1, 2016, Happy Tubs sold a hot tub to Monica,receiving a two-year, noninterest-bearing note in exchange for ahot tub that normally sells for $8,000. The note is for an amountthat achieves an effective interest rate of 10% per year.

Required:

1. Prepare the journal entry to record the sale.

2. Prepare any adjusting entry necessary on December 31, 2016. 3.Prepare any adjusting entry necessary on December 31, 2017.