ECON 2010 Lecture Notes - Lecture 23: Average Cost, Marginal Cost, Marginal Product

46

ECON 2010 Full Course Notes

Verified Note

46 documents

Document Summary

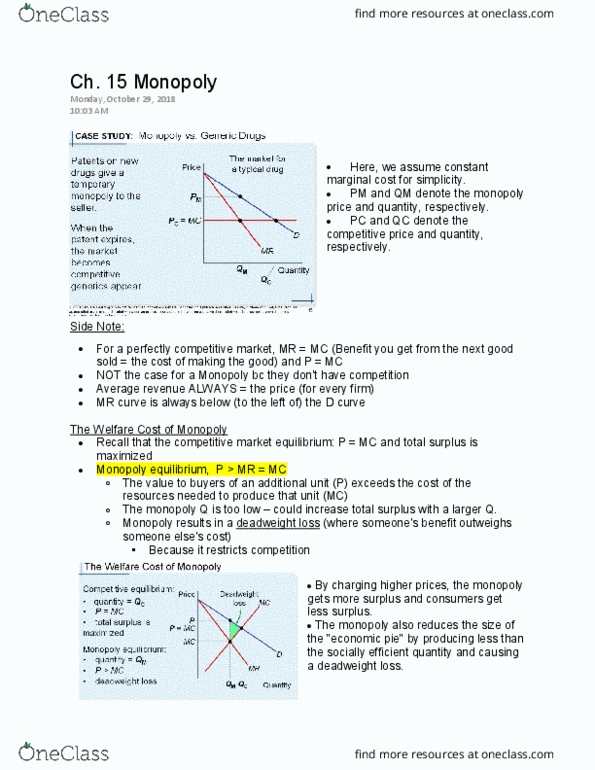

Diminishing marginal product is the same as increasing marginal cost. If marginal costs are increasing, every additional unit of output costs more than the previous one, so average variable costs are increasing. Average total cost is a u shaped curve. When quantity is low marginal cost is also low. Average total cost decreases at first but then bottoms out and increases with marginal cost. If mcatc, then average total cost is increasing. If mc=atc, then average total cost is at its minimum (efficient scale of production) Long run is however long it takes for a business to shut down and do something different (i. e. not signing a lease). All implicit costs are fixed in the short run but not in the long run. Economies of scale is when the long run average total cost decreases as quantity decreases. Diseconomies of scale is when the long-run average total cost increases as quantity increases.