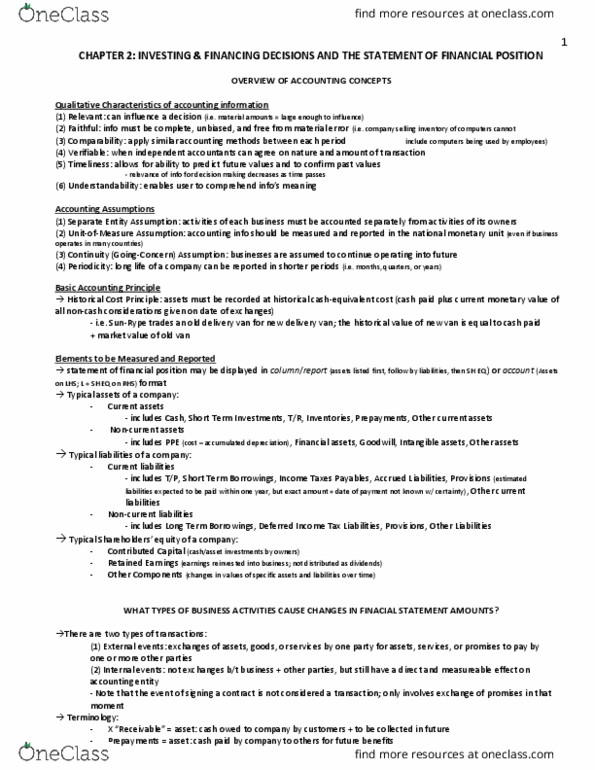

ACCT 110 Lecture Notes - Lecture 2: Historical Cost, Going Concern, Balance Sheet

30 May 2018

School

Department

Course

Professor

Week 2

Chap 1: continue

1. Events 5: assets is decreased so decrease stockholder equity

a. Revenue (sales)-expenses= net income(earning or profit)

1. Events 6: assets is decreased so decrease stockholder equity

1. Type of transaction

a. The described transaction has been classified in three categories

a. Assest source

a. Assets exchange

a. Assest use

1. Historical cost- requires that most asses be reported at the amount paid for them

1. Reliability concept- information is reliable if it can be independently verified.

Appraised value differs.

1. Accounting only care about historical cost

1. Creditors have priority

a. Lender get paid first

1. Going concern- assume the business will be able to operate until something comes

up

1. Permanent and temporary accounts

a. Permanent- financial track for years to years (ALE)

a. Temporary- financial tracked for limited time (RENI)

1. Annual- a book for every year

a. Finacial statements

a. Notes

a. Auditors report (is the editors)

a. Management's discussion and analysis (MD/D)

1. Balance sheet

a. A snapshot of a business position at certain time

a. Will list assets in order off liquidity?

1. Account Receivables

a. What your customers owes you

a. Also known as A/R

1. Liabilities

a. Short time- within 1 year

a. long term- more than 1 year

a. Bond payable

i. Not with a bank

i. With private investor

find more resources at oneclass.com

find more resources at oneclass.com