ACC 336 Lecture Notes - Lecture 3: Direct Labor Cost, Income Statement, Financial Statement

10 Jun 2020

School

Department

Course

Professor

Document Summary

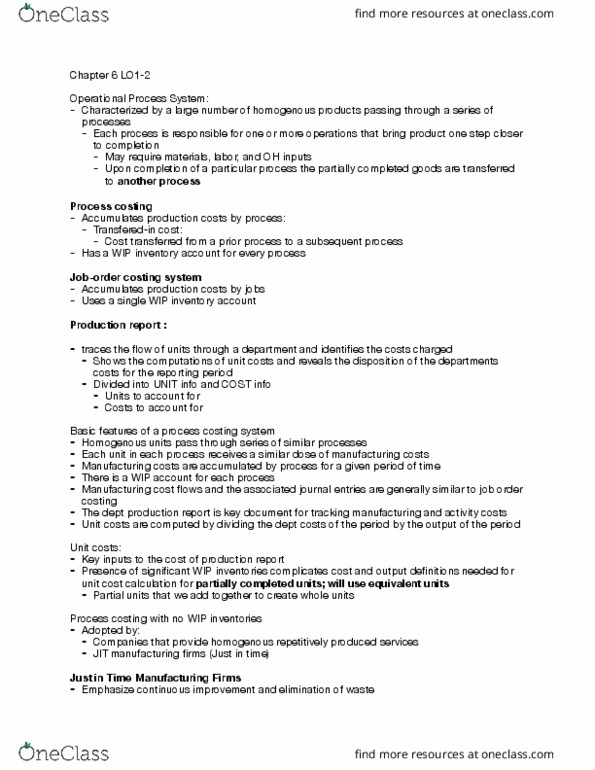

Services di er from tangible products on the following dimensions: Inseparability: producers of services and buyers of services must usually be in direct contact for an exchange to take place. Value chain: product costs - research& development, production, marketing, customer. Service - managerial objectives served - pricing decisions, product mix decisions, strategic pro tability analysis. Operating product costs - production, marketing, customer service - managerial objectives served - strategic design decisions, tactical pro t analysis. Tradition product costs - production - managerial function - external nancial reporting. Production (or product costs): costs associated with manufacturing goods or providing. Non production costs: costs associated with the functions of selling and admin services. Direct materials - traceable to the g/s being produced. Direct labor - labor that is traceable to the g/s produced. Overhead - production costs other than direct materials and direct labor.