ECON 1100 Lecture Notes - Lecture 1: Marginal Cost, Marginal Utility, Market Economy

13 Dec 2016

School

Department

Course

Professor

SEPTEMBER 1, 2016

ECONOMICS

- The study of how society manages its resources

- Economists study:

• How people make decisions

• How people interact with one another

• Analyze forces and trends that affect the economy as a whole

10 PRINCIPLES OF ECONOMICS

- How people make decisions

1. People face trade-offs

- People need to decide between one goal against another

- You lose something in exchange for one thing bcos resources are limited

- Ex. Studying vs. fun, national defense vs. standard of living in nations, protecting the

environment vs. profit

2. The cost of something is what you give up to get it

- Bcos people face trade-offs, they need to make decisions based on the cost and benefits of

alternatives

- Ex. Going to college

o Benefits: better jobs/opportunities and intellectual enrichment

o Costs: time, tuition, extra expenses

▪ Opportunity cost: whatever must be given up to obtain some item

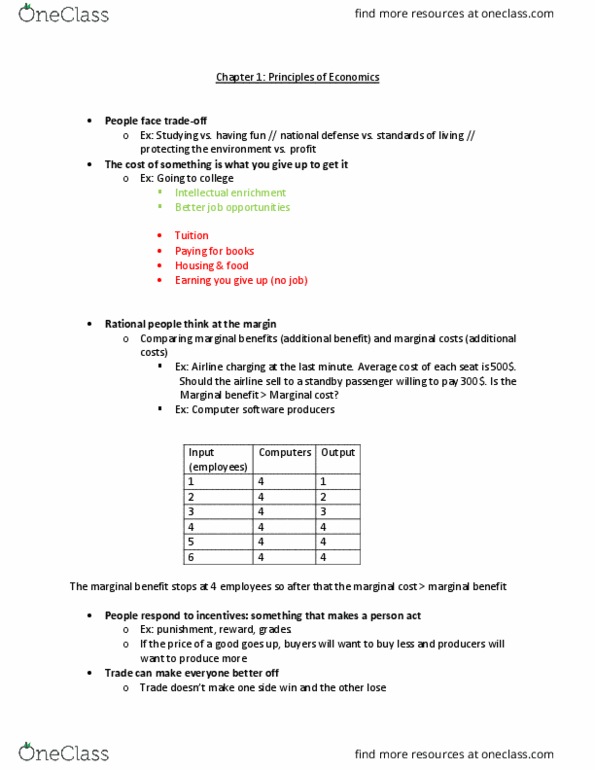

3. Rational people think at the margin

- Rational people make decisions by comparing marginal benefits (additional benefits) and

marginal costs (additional costs)

o People who systematically do the best they can to achieve their objectives

- Marginal change: a small adjustment to a plan of action

- Ex. Airline charging last minute. Average cost of each seat is $500. Should the airline sell to a

standby passenger willing to pay $300? Is the marginal benefit greater than the marginal cost?

Yes, the airline should charge bcos this will lessen the loss of the owner. Yes, the marginal

benefit is greater than the marginal cost.

4. People respond to incentives

- Incentive: something that drives/induces a person to act; ex. punishment, rewards, grades

- Ex. when prices of a commodity go up consumers want to buy less and sellers want to sell more

- How people interact

5. Trade can make everyone better off

- Trade is not a zero sum game where one side gains and the other loses

- Trade allows each person to specialize in the activities he or she does best

- Enjoy a greater variety of goods and services at a lower cost

- Specializing: a country specializes in its abundant resources

6. Markets are usually a good way to organize economic activity

- Market economy: relocates/allocates resources; where firms and households interact for goods

and services

- Central planning: government officials allocate the economy’s scarce resources (communist

countries)

- Adam Smith

find more resources at oneclass.com

find more resources at oneclass.com

• 1776, “Wealth of Nations”

• households and firms interact in markets bcos of self-interest

• conceptualized the “invisible hand” which leads to desirable outcomes

7. The government can sometimes improve market outcomes

- Why we need the government:

a) To enforce the rules and maintain institutions (ex. property rights)

o Ability of an individual to own and

exercise control over scarce resources

b) To prevent market failures

o When the market, left on its own, fails to allocate resources efficiently

o Causes:

i. Externalities

- Impact of one person’s actions on the well-being of bystanders (ex.

pollution)

ii. Market power

- Ability of a single economic actor to have a substantial influence on

market prices (ex. monopoly)

c) To intervene in the disparities in economic well-being

- The invisible hand doesn’t ensure that everyone has sufficient food, decent clothing, and

adequate health care

- Government intervention may diminish inequality

- How the economy as whole works

8. A country’s standard of living depends on its ability to produce goods and services

- There are very large differences in living standards around the world

• Ex. 2011, GDP of US: $48,000 and GDP of Nigeria: $1,200 bcos difference in production

- Production: the quantity of goods and services produced from each unit of labor input

- The growth rate of a nation’s productivity determines the growth rate of its average income

9. Prices rise when the government prints too much money

- Inflation: an increase in overall level of prices in the economy

- Usually the reason is growth in the quantity of money

- Printing too much = value of money falls

10. Society faces a short-run trade-off between inflation and unemployment

- The short-run effect of monetary injunction is that it stimulates the overall of spending which causes firms to

hire more workers and produce more but it also induces inflation

SEPTEMBER 8, 2016

ECONOMICS

- Divided between:

1. Microeconomics

- The study of how households and firms make decisions and how they interact in markets

2. Macroeconomics

- The study of economy-wide phenomena, including inflation, unemployment, and economic

growth

- Follows a scientific method

• Observations help to develop theories

• Data can be collected and analyzed to evaluate theories

find more resources at oneclass.com

find more resources at oneclass.com

• Using data to evaluate theories is more difficult in economics than in physical science bcos economists

are unable to generate their own data and must make do with whatever data are available

• Thus, economists pay close attention to the natural experiments offered by history

- Economic Models

• Used to learn about the real world

• Mostly consists of diagrams and equations

• All models simplify reality to improve our understanding of it

- The Role of Assumptions

• Simplify the complex world and make it easier to understand

• Focus our thinking on the essence of the problem

• Economists often use assumptions that are unrealistic but will have small effects on the actual outcome

of the answer

PRODUCTION POSSIBILITY FRONTIER

- An economic model

- A graph that shows the combinations of output that the economy can possibly produce given the available

factors of production and the available production technology

- Assumptions:

• The economy only produces 2 goods (e.g. cars and computers)

• Factors of production and technology do not change

• If all resources are devoted to producing cars, the economy would produce 1,000 cars and 0 computers

• If all resources are devoted to producing computers, the economy would produce 3,000 computers and 0

cars

- Ex.

Computers

A, B – the economy divides its resources between two industries

C – the economy can’t produce at this point bcos resources are scarce/not enough resources

D – inefficient point of production (bcos you have resources but you you’re not using it)

*any point on the PPF curve is efficient

Cars

3000

- - - - - - - - - - -

- - - - - - - - - - - - - - - - -

- - - - - - - - - - - - -

- - - - - - - - - - - - - -

- - - - - - -

- - - - - -

2200

2000

700

300

600

1000

1000

A

B

C

D

find more resources at oneclass.com

find more resources at oneclass.com