ACCT 203 Lecture Notes - Lecture 24: Balanced Scorecard

25 May 2018

School

Department

Course

Professor

GMU ACCOUNTING 203 Lecture 24

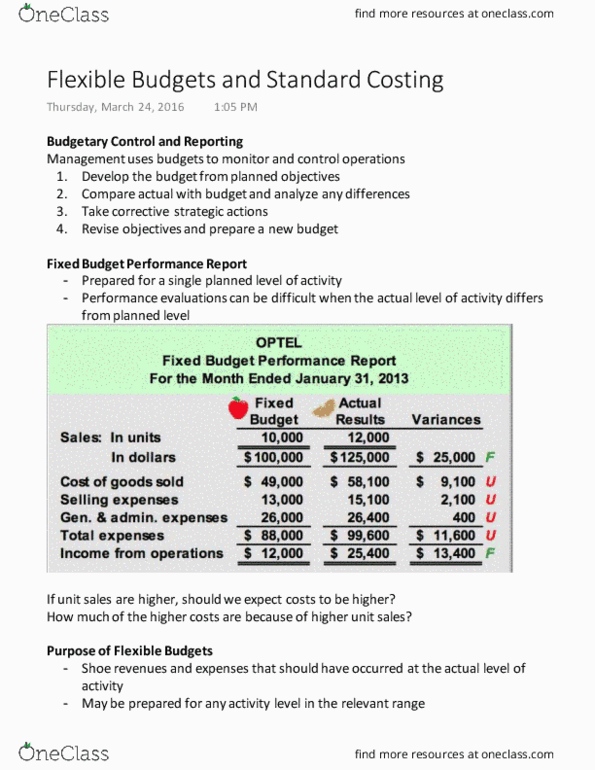

Budget performance report

A report comparing actual results with budget figures.

Budgeted variable factory overhead

The standard variable overhead for the actual units produced.

Controllable variance

The difference between the actual amount of variable factory overhead cost

incurred and the amount of variable factory overhead budgeted for the standard

product.

Cost variance

The difference between actual cost and the flexible budget at actual volumes.

Currently attainable standards

Standards that represent levels of operation that can be attained with reasonable

effort.

Direct labor rate variance

The cost associated with the difference between the standard rate and the actual

rate paid for direct labor used in producing a commodity.

Direct labor time variance

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

A report comparing actual results with budget figures. The standard variable overhead for the actual units produced. The difference between the actual amount of variable factory overhead cost incurred and the amount of variable factory overhead budgeted for the standard product. The difference between actual cost and the flexible budget at actual volumes. Standards that represent levels of operation that can be attained with reasonable effort. The cost associated with the difference between the standard rate and the actual rate paid for direct labor used in producing a commodity. The cost associated with the difference between the standard hours and the actual hours of direct labor spent producing a commodity. The cost associated with the difference between the standard price and the actual price of direct materials used in producing a commodity. The cost associated with the difference between the standard quantity and the actual quantity of direct materials used in producing a commodity.