ACCT 203 Lecture Notes - Lecture 13: Trial Balance, Retained Earnings, Income Statement

Document Summary

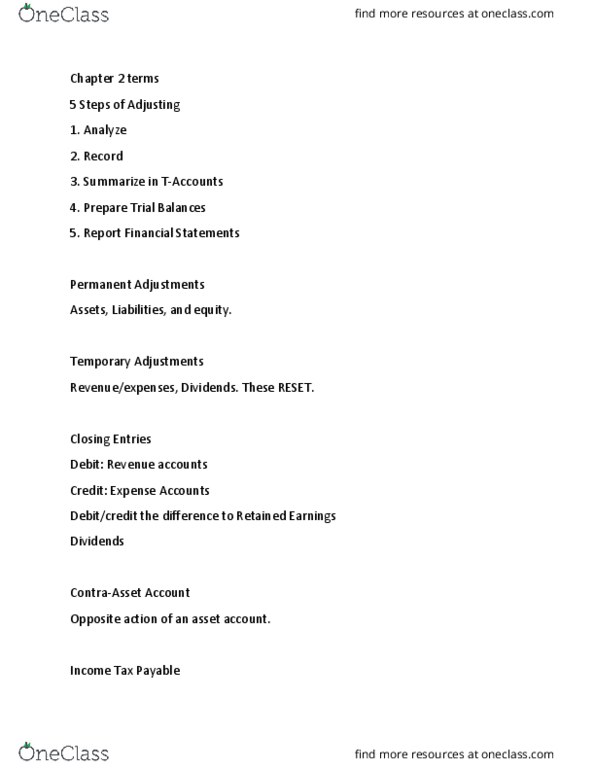

Trial balance and adjusted trial balance: print an unadjusted trial balance, review the unadjusted trial balance and prepare adjusting journal entries to correct for any transactions missed or incorrectly recorded. Adjusting prepaids, unearned revenue, depreciation expense, allowance for bad debts, etc are all common items that are captured with adjusting entries: print an adjusted trial balance. Repeat the process again if necessary to capture any issues and record adjusting entries as needed: prepare the closing entries which eliminate the balance in the income statement accounts (ie. revenue and expense accounts) . Temporary accounts so at the end of each period they are. Reversed to zero and the balance goes to income summary. Account which is then closed to retained earings. Therefore, you debit the revenue accounts and credit the expense accounts to get them to go to zero. The difference is a plug to income summary (and also is by definition your net income or loss).